Scarcity and Economic Activities

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Introduction to Scarcity

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we'll explore the concept of scarcity. Can anyone tell me what they understand by scarcity?

Isn't scarcity when there isn’t enough of something?

Exactly! Scarcity refers to the limited availability of resources to meet unlimited wants. This means we have to make choices about how to use our resources effectively. Can someone provide an example of this in their life?

When my parents go shopping, if they have a limited budget, they can't buy everything on the list.

Great example! That's a perfect illustration of how scarcity forces us to prioritize our needs.

Economic Activities Defined

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's talk about the different roles people play in the economy. Who can tell me what a consumer is?

A consumer is someone who buys goods or services?

That's right! Consumers aim to satisfy their wants through purchasing. Now, what about producers?

Producers create goods or services, right?

Exactly! Producers utilize resources to meet consumer needs. Additionally, we have employees who work for others and earn wages. Remember the acronym 'CPE' — Consumer, Producer, Employee. It helps us remember these key economic roles!

Scarcity and Choices

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

With limited resources, how do you decide what to buy?

I prioritize what I want the most based on my budget.

Yes! This is where opportunity cost comes in. It’s the cost of the next best alternative you give up when making a choice. Can anyone think of a time they faced opportunity cost?

Once I had to choose between buying a video game and saving for a new phone.

Perfect example! You had to weigh the benefits of each option. Remembering opportunity costs is key!

Link Between Statistics and Economics

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Why do you think statistics is important in economics?

Maybe to understand trends and make predictions?

Absolutely! Statistics helps us analyze data related to economic activities and understand changes in consumption, production, and distribution. For instance, how might statistics help a government plan for future economic needs?

They could forecast what people will need, like in healthcare or housing.

Exactly! Forecasting through statistics is crucial in making sound economic policies. Always think of the acronym 'A.P.P.' - Analyze, Predict, Plan!

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

Scarcity, defined as the limited nature of resources, creates economic problems that require choices in consumption, production, and distribution. The section emphasizes that economic activities aim for monetary gain and how understanding statistics can elucidate these activities.

Detailed

Scarcity and Economic Activities

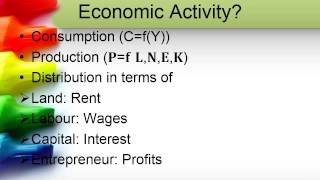

This section explores the fundamental concept of scarcity in economics, described as the limited availability of resources in contrast to unlimited human wants. Alfred Marshall's definition positions economics as the study of human behavior in fulfilling needs through various economic activities: consumption, production, and distribution. In everyday life, people engage in economic activities based on their roles—consumers, producers, employees, and employers—all driven by monetary gain.

The section emphasizes that scarcity necessitates choices; individuals cannot satisfy all their wants due to limited resources and must prioritize those they value most. The ongoing reality of scarcity is illustrated through relatable scenarios, such as managing limited pocket money or facing price increases. The economic factors involved in consumption, production, and distribution require the analysis of data, reinforcing the role of statistics in comprehending economic behavior. The interconnection between economics and statistics is highlighted, emphasizing the need for data in formulating sound economic policies and addressing societal issues like poverty and income disparity.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Understanding Scarcity

Chapter 1 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Scarcity is the root of all economic problems. Had there been no scarcity, there would have been no economic problem. And you would not have studied Economics either.

Detailed Explanation

Scarcity refers to the limited availability of resources to meet unlimited wants. It is a fundamental concept in economics because it drives the need for choices. If resources like money, time, or goods were unlimited, there would be no need to allocate them wisely or make decisions regarding their use.

Examples & Analogies

Imagine if everyone had a magic wallet that replenishes money whenever you spend it. In that world, there would be no need to think about how you spend money because it's never going to run out. However, in reality, we must prioritize our spending because our income is limited.

Manifestations of Scarcity

Chapter 2 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

In our daily life, we face various forms of scarcity. If you ever heard the story of Aladdin and his Magic Lamp, you would agree that Aladdin was a lucky guy. Whenever and whatever he wanted, he just had to rub his magic lamp. But in real life, we do not have such luxuries.

Detailed Explanation

While the story of Aladdin depicts a life without scarcity, our reality is filled with examples of limited resources. Everyday experiences—like waiting in long lines, budgeting expenses, or making choices between wants—demonstrate how we deal with scarcity. Each choice we make reflects our priorities based on our limited resources.

Examples & Analogies

Think of a scenario like planning a birthday party. You might want to invite many friends, buy plenty of decorations, or have a big cake. However, if your budget only allows for a simple party with fewer guests, you need to make choices about what aspects of the party are most important.

Economic Activities Defined

Chapter 3 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Economic activities are actions undertaken for monetary gain. This includes consumption, production, and distribution. When you buy goods, you are a consumer; when you sell goods, you are a seller; when you produce goods, you are a producer.

Detailed Explanation

Economic activities encompass all actions that contribute to the production, distribution, and consumption of goods and services. Being a consumer means purchasing to meet your and your family's needs. Being a seller involves offering goods or services to make a profit. Producers engage in creating goods or services, thereby fulfilling the needs of consumers.

Examples & Analogies

Consider a local farmer. They grow vegetables (production), sell them at a market (distribution), and consumers buy them (consumption). Each of these actions is essential for the economy to function and reflects the roles of different economic participants.

Resource Allocation and Choices

Chapter 4 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Scarcity forces us to make choices about how we allocate our limited resources. Resources like land, labor, and capital have alternative uses. This leads to choices between products that can be produced.

Detailed Explanation

Because resources are scarce, we cannot produce everything we desire. For example, a piece of farmland can be used to grow crops or raise livestock, but not both simultaneously. Therefore, when we decide to produce one over the other, we are making a choice based on our priorities and expected benefits.

Examples & Analogies

Imagine having a small garden where you can either plant tomatoes or strawberries. If you choose tomatoes because they sell for a higher price at the market, you must forgo the strawberries. Your decision showcases the concept of opportunity cost, a crucial aspect of economics.

Statistics and Economics

Chapter 5 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Statistics helps us understand economic activities by providing reliable facts about consumption, production, and distribution. It allows economists to analyze real-life economic problems and formulate policies to address them.

Detailed Explanation

Statistics is vital in economics because it equips economists with the data needed to identify trends, make forecasts, and formulate strategies based on empirical evidence. For instance, understanding how consumer spending rises with increases in average income comes from analyzing statistical data.

Examples & Analogies

Consider a local café observing statistics about customer behavior. If they find that sales increase every December due to holiday spirit, they might decide to introduce new festive menu items. This use of data illustrates how statistics inform economic decisions.

Key Concepts

-

Scarcity: The limited availability of resources.

-

Opportunity Cost: The cost of giving up the next best alternative when making a choice.

-

Economic Activities: Actions related to consumption, production, and distribution for monetary gain.

-

Role of Statistics: Essential for analyzing economic data and formulating policies.

Examples & Applications

An example of scarcity is a student having only $10 to spend on food and having to choose between a sandwich and a drink.

An example of opportunity cost is prioritizing study time over leisure activities to ensure better exam results.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

Scarcity creates a choice, by limiting what you can voice.

Stories

Imagine a small island with limited food resources. The islanders must choose between planting crops or fishing, teaching them about scarcity and making decisions.

Memory Tools

CPE - Remember Consumer, Producer, Employee roles in the economy.

Acronyms

A.P.P. - Analyze, Predict, Plan when using statistics in economics.

Flash Cards

Glossary

- Scarcity

The limited nature of resources in comparison to the limitless human wants.

- Opportunity Cost

The loss of potential gain when one alternative is chosen over another.

- Consumer

An individual who purchases goods and services to satisfy their wants.

- Producer

An individual or entity that creates goods or services.

- Employee

An individual who is in a paid position working for someone else.

Reference links

Supplementary resources to enhance your learning experience.