Central Problems of an Economy

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Scarcity and Economic Problems

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today we're going to discuss why scarcity is at the heart of economic problems. Scarcity forces economies to make choices about resource allocation.

So, scarcity means there are limited resources available?

Exactly! Because of scarcity, we must decide what to produce, how to produce it, and for whom we are producing.

Can you explain what you mean by 'what to produce'?

Certainly! It means an economy must decide between various goods—like food, clothing, or technology—and in what quantities they should be produced.

What if the demand for a good changes?

Great question! If demand changes, the economy must reevaluate its production strategies to align with consumer preferences.

To recap, scarcity leads us to make economic decisions about production and resource use. Any questions before we move on?

How to Produce

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Next, we will explore how societies decide to produce their goods. Should they use more machines or more labor?

What determines that choice?

It's influenced by the available resources and the technology accessible—a society might prefer labor for certain goods and machines for others.

So the production methods can vary depending on the situation?

Exactly! Each method has different costs and outputs, so it's crucial to analyze what fits best given those circumstances.

To summarize this session, choosing production methods is driven by resource availability and technology. Can anyone name a production method?

Like assembly lines in factories?

Correct! Well done!

For Whom to Produce

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now let's tackle the final question: 'For whom are these goods produced?' This revolves around resource distribution.

Does that mean deciding which groups get access to what resources?

Yes, exactly! It's about equity and access. We must consider how resources should be distributed among individuals and groups.

How do economies ensure fair distribution?

Good question! Some economies use policies to promote equality, while others rely solely on market forces.

To summarize today, we’ve covered the three core economic problems that arise due to scarcity: what to produce, how to produce, and for whom to produce. Any final thoughts?

Production Possibility Frontier

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now that we understand the fundamental problems, let's introduce the concept of the Production Possibility Frontier or PPF.

What is a PPF?

It represents the maximum output possibilities for two goods, showing trade-offs and opportunity costs.

Could you give an example?

Sure! If an economy can produce either corn or cotton, the PPF will show combinations of both that can be produced, illustrating opportunity costs.

So, if we want more corn, we give up some cotton. Remember, this trade-off is crucial for any economy!

How do we visualize this?

We plot it on a graph, with one good on each axis. Any point along the curve shows efficient production!

To conclude, understanding the PPF is essential for recognizing the trade-offs involved in resource allocation.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

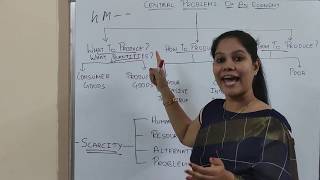

The section outlines three primary economic questions that every society must address: what to produce, how to produce, and for whom to produce, emphasizing the role of resource scarcity in decision-making.

Detailed

In every economy, the key activities revolve around production, exchange, and consumption of goods and services. Scarcity of resources leads to difficult choices regarding how to allocate these limited resources effectively. The economic problems can be summarized into three fundamental questions: 1) What goods and services to produce and in what quantities? 2) How should these goods be produced, considering the balance between labor and technology? 3) For whom are these goods produced, determining the distribution of resources among individuals? The section also highlights the concept of a Production Possibility Frontier (PPF), which illustrates different combinations of goods that can be produced, emphasizing the opportunity cost of choices made by an economy. Understanding these central problems is crucial for optimizing resource allocation and ensuring the economy meets the needs of its population.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Overview of Economic Activities

Chapter 1 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Production, exchange and consumption of goods and services are among the basic economic activities of life. In the course of these basic economic activities, every society has to face scarcity of resources and it is the scarcity of resources that gives rise to the problem of choice.

Detailed Explanation

This section introduces the primary economic activities that every society engages in, which include production (creating goods and services), exchange (trading those goods and services), and consumption (using the goods and services). Scarcity refers to the fundamental issue that resources are limited, and this situation poses a challenge regarding which choices should be made. Essentially, because resources cannot satisfy all wants, societies must make decisions about how to allocate what they have.

Examples & Analogies

Imagine you have a limited amount of money to spend on groceries. You can either buy healthy food, snacks, or drinks. However, you cannot afford to buy all of them. Hence, you have to make a choice about which ones to purchase, similar to how economies face choices with limited resources.

What to Produce?

Chapter 2 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Every society must decide on how much of each of the many possible goods and services it will produce. Whether to produce more of food, clothing, housing or to have more of luxury goods. Whether to have more agricultural goods or to have industrial products and services. Whether to use more resources in education and health or to use more resources in building military services.

Detailed Explanation

The first central economic problem is about deciding what to produce. Societies have to make choices concerning the quantity and types of goods and services to produce. This requires weighing the benefits of producing necessities like food and clothing against luxury items, or deciding between investing in sectors like education or military. Every decision involves trade-offs, as resources are allocated to one choice, which limits production of another.

Examples & Analogies

Consider a local bakery deciding whether to make more bread (a basic necessity) or pastries (a luxury good). If they choose to make more bread, they must allocate less time and ingredients to pastries, showing how choices have direct consequences on what is available in the market.

How to Produce?

Chapter 3 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Every society has to decide on how much of which of the resources to use in the production of each of the different goods and services. Whether to use more labour or more machines. Which of the available technologies to adopt in the production of each of the goods?

Detailed Explanation

The second problem focuses on the 'how' of production. Societies need to decide the combination of resources to produce goods and services. This includes choosing the ratio of labor to machines and deciding which technologies to implement. These choices can affect efficiency, costs, and the quality of the goods produced.

Examples & Analogies

Imagine a car manufacturing company. It must choose whether to hire more workers to assemble cars or invest in advanced robotics to automate part of the assembly process. Each choice has implications for production speed, cost, and ultimately the type of car they can produce.

For Whom to Produce?

Chapter 4 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Who gets how much of the goods that are produced in the economy? How should the produce of the economy be distributed among the individuals in the economy?

Detailed Explanation

The final economic problem is about distribution, specifically how the goods and services produced are allocated among individuals in society. This encompasses questions of equity and fairness—who receives what, how much they receive, and whether everyone has access to basic needs like food and education.

Examples & Analogies

Think of a community garden where the vegetables grown must be shared among the community members. Questions arise about who gets which portions: should it be equal for everyone, or should families with more children receive a larger share? This reflects the complexities of fair distribution in an economy.

The Concept of Opportunity Cost

Chapter 5 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Thus, there is always a cost of having a little more of one good in terms of the amount of the other good that has to be forgone. This is known as the opportunity cost of an additional unit of the good.

Detailed Explanation

Opportunity cost is a vital concept in economics that refers to the value of the next best alternative that is given up when a choice is made. Since resource allocation involves trade-offs, understanding opportunity costs helps individuals and societies evaluate decisions and their impacts on resource usage and welfare.

Examples & Analogies

If you decide to spend your evening studying for an exam rather than going out with friends, the opportunity cost is the enjoyment and relaxation you sacrifice by not socializing. This concept is similarly applicable when economies make decisions regarding production.

Key Concepts

-

Scarcity: Limited resources lead to difficult economic choices.

-

Production: Creating goods and services.

-

Exchange: Trading goods and services.

-

Consumption: Use of produced goods.

-

Production Possibility Frontier (PPF): Illustrates trade-offs between two goods.

-

Opportunity Cost: The cost of the next best alternative.

Examples & Applications

If a family has limited funds, it must decide whether to buy groceries or save for a new phone, showcasing the concept of opportunity cost.

A factory may face the choice of producing more cars or more bicycles, illustrating the PPF concept with potential trade-offs.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

Scarcity means choice, that's no surprise; make good decisions, open your eyes!

Stories

Imagine a town with limited water. Each family has to decide how to use it: drinking, washing, or irrigation. This demonstrates scarcity and decision-making.

Memory Tools

To remember the core economic problems: 'P-C-D' (Production, Choice, Distribution).

Acronyms

PPF

'Producing Perfectly Finite' resources.

Flash Cards

Glossary

- Scarcity

The limited availability of resources relative to the unlimited wants of individuals and societies.

- Production

The process of creating goods and services using resources.

- Exchange

The act of trading goods or services between parties.

- Consumption

The use of goods and services by individuals or groups.

- Production Possibility Frontier (PPF)

A graph that shows the maximum feasible amount of two goods that can be produced with available resources.

- Opportunity Cost

The cost of forgoing the next best alternative when making a decision.

Reference links

Supplementary resources to enhance your learning experience.