Equilibrium, Excess Demand, Excess Supply

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Understanding Market Equilibrium

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Good morning class! Today, we'll explore the concept of market equilibrium. To start, can anyone tell me what we mean by equilibrium in a market context?

Isn't it when the amount people want to buy equals what firms want to sell?

Exactly, Student_1! Equilibrium occurs when the quantity supplied matches the quantity demanded, resulting in a stable market price. This is represented as (p*, q*).

What happens if there’s more supply than demand?

Great question! When supply exceeds demand, we have excess supply, which usually leads to lower prices as firms try to sell their excess goods.

And excess demand occurs when the opposite happens, right?

Absolutely! In that case, prices tend to rise until equilibrium is restored. Remember, we refer to this adjustment mechanism as the 'invisible hand' of the market.

What are the implications of these shifts?

That's crucial for understanding market dynamics. A shift in demand or supply can significantly affect equilibrium prices and quantities. Always think about how these shifts interact!

To recap today’s session, market equilibrium is achieved when supply equals demand, and adjustments occur due to excess supply or demand.

Effects of Demand and Supply Shifts

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's now examine what happens when there is a shift in demand. Can someone explain what a rightward shift in the demand curve indicates?

It means that at every price point, consumers want to buy more of the product.

Correct, Student_1! This shift typically raises both equilibrium price and quantity. Are there any other factors that could cause a shift in demand?

Changes in consumer income or tastes!

Spot on! Changes in consumer income can cause demand to increase for normal goods and decrease for inferior goods. Now, what about supply shifts? What happens when the supply curve shifts to the left?

That usually means firms are willing to supply less at all prices, which might lead to an increase in price.

Exactly! If supply decreases while demand remains unchanged, prices will rise and equilibrium quantity will fall. Always remember, the relationship between shifts and equilibrium is paramount.

To summarize, shifts in demand generally affect both equilibrium price and quantity, while shifts in supply affect them in opposite directions. Understanding these dynamics is essential in market analysis!

Role of the Invisible Hand

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now, let's touch upon the concept of the 'invisible hand.' How does this metaphor relate to market equilibrium?

It suggests that individuals pursuing their own interests can lead to the best outcomes for society.

Exactly! Adam Smith introduced this concept, proposing that market forces naturally regulate prices. This self-correcting behavior keeps the market balanced. What happens when there’s excess demand due to a price drop?

Prices will rise until it reaches equilibrium again.

Yes! This dynamic ensures the market remains efficient. Can someone summarize the significance of the invisible hand?

It shows how individual actions can lead to economic stability and optimal resource allocation.

Perfectly summarized, Student_3. To conclude this session, the 'invisible hand' is a powerful concept in economics representing the self-regulating nature of the market.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

The section explains how market equilibrium is established when consumer demand equals firm supply. It discusses the conditions for excess demand and supply, the role of the 'invisible hand' in price adjustments, and how shifts in demand and supply curves affect market outcomes.

Detailed

Detailed Summary

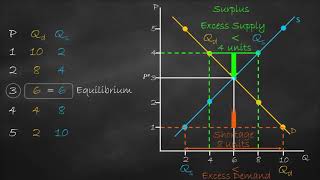

In a perfectly competitive market, equilibrium occurs when the plans of consumers align with the intentions of firms, resulting in no excess demand or supply. The equilibrium price (p*) is the price at which the quantity demanded by consumers (qD) equals the quantity supplied by firms (qS).

Key Points:

- Market Equilibrium Definition: Equilibrium is reached when market demand equals market supply at a specific price and quantity (p, q).

- Excess Demand and Supply: If the market supply exceeds demand at a price, there’s excess supply; conversely, if the demand exceeds supply, there’s excess demand.

- Role of the 'Invisible Hand': According to classical economics, market forces naturally adjust prices towards equilibrium in response to excess demand or supply.

- Shifts in Demand and Supply: Changes in consumer preferences, income levels, or the number of firms affect market equilibrium, leading to price adjustments. For instance, a rightward shift of the demand curve leads to higher equilibrium prices and quantities, while a leftward shift causes the opposite.

This section is crucial for understanding how markets balance under different conditions and the implications of shifts in demand and supply.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Introduction to Market Equilibrium

Chapter 1 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

A perfectly competitive market consists of buyers and sellers who are driven by their self-interested objectives. Recall from Chapters 2 and 4 that objectives of the consumers are to maximise their respective preference and that of the firms are to maximise their respective profits. Both the consumers’ and firms’ objectives are compatible in the equilibrium.

Detailed Explanation

In a perfectly competitive market, individuals act out of self-interest — consumers want to buy at the lowest price possible, while firms want to sell at the highest price possible. This self-interested behavior leads to a situation known as market equilibrium, where the supply of goods matches demand. At this point, both consumers and firms are satisfied as they achieve their objectives without any excess supply or demand.

Examples & Analogies

Imagine a busy marketplace where many people are trying to buy fresh fruits. Sellers want to maximize their prices while buyers want to get the best deals. When sellers set a price that allows all fruits to be sold without leftovers, and all buyers have found what they want, the market reaches equilibrium. It signifies balance — no one wants to change their price because they are satisfied with the exchange.

Defining Equilibrium

Chapter 2 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

An equilibrium is defined as a situation where the plans of all consumers and firms in the market match and the market clears. In equilibrium, the aggregate quantity that all firms wish to sell equals the quantity that all the consumers in the market wish to buy; in other words, market supply equals market demand. The price at which equilibrium is reached is called equilibrium price and the quantity bought and sold at this price is called equilibrium quantity.

Detailed Explanation

Equilibrium occurs when the amount of goods that firms are prepared to sell is equal to the amount that consumers want to buy. This is reflected in two key terms: the equilibrium price, which is the price at which this balance occurs, and the equilibrium quantity, which is the quantity of goods exchanged at that price. When either of these conditions isn’t met, adjustments will occur in the market until a new equilibrium is established.

Examples & Analogies

Consider a popular concert where tickets are priced at $50. If 1,000 people want to buy tickets, but only 800 are available, that leads to excess demand. The concert organizers may raise the ticket price until the new quantity demanded matches the supply — perhaps to $60 — achieving a new equilibrium where 800 people are willing to buy at this price.

Understanding Excess Demand and Excess Supply

Chapter 3 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

If at a price, market supply is greater than market demand, we say that there is an excess supply in the market at that price and if market demand exceeds market supply at a price, it is said that excess demand exists in the market at that price. Therefore, equilibrium in a perfectly competitive market can be defined alternatively as zero excess demand-zero excess supply situation.

Detailed Explanation

Excess demand occurs when the quantity demanded by consumers at a given price exceeds the quantity supplied by producers. Conversely, excess supply occurs when producers supply more than what consumers are willing to buy. These situations prompt natural market adjustments — with excess demand causing prices to rise and excess supply leading to price drops until the market reaches a new equilibrium.

Examples & Analogies

Think of a situation in a bakery where fresh bread is sold. If on a certain day they bake 200 loaves but 300 people are queued up to buy them, there’s excess demand. The bakery might raise prices for the next batch to balance supply and demand. If they bake 300 loaves the following day and only 200 people come, that creates excess supply, prompting the bakery to lower prices to attract more customers.

Invisible Hand and Pricing Dynamics

Chapter 4 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Whenever market supply is not equal to market demand, and hence the market is not in equilibrium, there will be a tendency for the price to change. In a perfectly competitive market, an ‘Invisible Hand’ is at play which changes price whenever there is imbalance in the market.

Detailed Explanation

The concept of the ‘Invisible Hand,’ proposed by economist Adam Smith, suggests that individuals’ self-interested actions inadvertently promote the welfare of society as a whole. In the context of market equilibrium, when there is a mismatch between supply and demand, market forces will adjust prices — raising them in the case of excess demand and lowering them in cases of excess supply — leading to a new equilibrium. This process reflects how markets naturally respond to changes.

Examples & Analogies

Picture yourself buying avocados at a supermarket. If a sudden trend makes avocados very popular, the demand skyrockets. Initially, the price might jump sharply as people are willing to pay more. Over time, as a result of higher prices, more suppliers start stocking avocados until the prices stabilize at a new equilibrium, balancing supply with the new level of demand.

Key Concepts

-

Equilibrium: The condition where quantity demanded equals quantity supplied.

-

Excess Demand: Occurs when demand for a good exceeds its supply.

-

Excess Supply: Occurs when supply of a good exceeds its demand.

-

Invisible Hand: The self-regulating behavior of the marketplace.

-

Market Demand and Supply: The total quantities of goods consumers are willing to buy and firms are willing to sell respectively.

Examples & Applications

If the market price of a good is low, the quantity demanded will increase while the supply may decrease, indicating excess demand.

On the other hand, if the price is set too high, the quantity supplied will surpass the quantity demanded, resulting in excess supply.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

When supply's low and demand's high, prices rise up to the sky!

Stories

Imagine a bustling marketplace where sellers flood in with products, but only a few buyers show interest; prices drop until everyone wants to buy, balancing the stalls!

Memory Tools

Remember E for Equilibrium, the balance where D meets S: Demand equals Supply!

Acronyms

ESED - Equilibrium signifies Supply = Demand, Excess Demand pushes prices up, Excess Supply pushes prices down.

Flash Cards

Glossary

- Equilibrium

A condition where market supply equals market demand.

- Excess Demand

A situation in which the quantity demanded exceeds the quantity supplied at a given price.

- Excess Supply

A situation in which the quantity supplied exceeds the quantity demanded at a given price.

- Invisible Hand

A metaphor introduced by Adam Smith to describe the self-regulating nature of the market.

- Market Demand

The total quantity of a good that all consumers in a market are willing to purchase at different prices.

- Market Supply

The total quantity of a good that all producers in a market are willing to sell at different prices.

Reference links

Supplementary resources to enhance your learning experience.