Payback Period (PBP)

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Introduction to Payback Period

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we’re discussing the Payback Period, or PBP. Can anyone tell me what they think it measures in capital budgeting?

Does it measure how long it takes to recover an investment?

Exactly! The payback period indicates how many years it will take for the initial investment to be returned through cash inflows. The formula we use is: payback period equals the initial investment divided by annual cash inflow.

Why is this important for companies?

Great question! It's particularly useful for assessing liquidity, which is crucial for companies that need to ensure they can cover their short-term financial obligations.

Are there any limitations to this method?

Yes, the payback period does ignore the time value of money, meaning cash flows in the future are viewed the same as those in the present. It also neglects any cash inflows after the payback period. These limitations can lead to potentially overlooking profitable projects.

So, it’s not the only measure we should use?

Correct! It’s a useful metric but should be used alongside other methods for a more comprehensive capital budgeting analysis.

In summary, the Payback Period helps companies evaluate the urgency of recovering their investments, but it has notable shortcomings that necessitate caution.

Calculating Payback Period

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

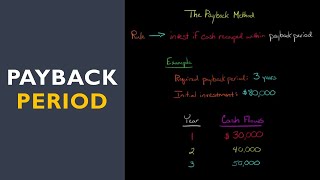

Let's delve into the calculation for the Payback Period. If a company invests $10,000 and expects annual cash inflows of $2,000, how would we find the payback period?

We would divide the initial investment by the annual cash inflow, right?

Exactly! So, that means: $10,000 divided by $2,000 gives us a payback period of 5 years.

Can we quickly tell if that’s a good investment?

While a 5-year payback could be acceptable for some companies, others may prefer to recoup their investments much faster, especially in rapidly changing industries.

What if the cash inflows were less every year? How would that affect the PBP?

Good thinking! Lower cash inflows would extend the payback period. It would take longer to recoup the initial investment, which could make the investment less attractive.

So cash flow consistency is important too?

Yes, consistency in cash inflows plays a critical role in evaluating any investment! Remember our acronym, PBP, 'Predicting Budgets Precisely.'

In summary, while calculating the Payback Period can give a quick assessment of liquidity, understanding the flow of cash inflows is crucial for making informed investment decisions.

Advantages and Disadvantages of PBP

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's review the advantages of using the Payback Period. What do you think?

It’s simple and easy to calculate?

That's right! It's one of its main advantages. Simple calculations improve our efficiency when assessing investments, especially in urgent situations.

What about the disadvantages? I remember you mentioned some.

Exactly, while it’s straightforward, it ignores the time value of money, which can lead to poor investment decisions. Plus, it misses any cash flows that occur after the payback period, which can also be significant.

What if we use it only for preliminary evaluations?

Using it as a preliminary measure is smart, but ensure to follow it up with other metrics that account for cash flow beyond the payback period.

So overall, it helps with quick evaluations, but can be misleading if used alone?

Precisely! The payback period offers quick insights but should be a part of a broader analysis strategy.

In summary, while the PBP is straightforward and beneficial for assessing liquidity, its limitations necessitate caution in relying on it as the sole evaluation metric.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

The Payback Period (PBP) is a traditional capital budgeting technique that determines the time it takes to recoup the initial investment. While it is straightforward and useful for assessing liquidity, it has limitations, including ignoring the time value of money and ignoring cash flows after the payback period.

Detailed

Payback Period (PBP)

The Payback Period (PBP) is a widely used traditional capital budgeting technique that measures the time it takes for an organization to recover its initial investment from the cash inflows generated by that investment. The payback period is a simple calculation that can provide valuable insights into the liquidity and risk associated with an investment project.

Formula

The PBP is calculated as:

Payback Period (PBP) = Initial Investment / Annual Cash Inflow

This formula represents how many years it will take to recover the amount invested with the cash flows expected from the project.

Advantages

- Simplicity: The calculation is straightforward and easy to understand.

- Liquidity Assessment: Helps determine how quickly the invested money can be retrived, making it ideal for firms concerned with cash flow.

Disadvantages

- Ignores Time Value of Money: The PBP does not take into account the diminishing value of cash in future years, which can mislead decision-making.

- Neglects Cash Flows Beyond the Payback Period: Once the payback period is reached, any future cash inflows are not factored into the decision process, which could lead to potential profitable investments being overlooked.

In the realm of capital budgeting, understanding the PBP is crucial for organizations, especially in technology sectors, where rapid changes in investments can lead to urgent decision-making about new projects or products.

Youtube Videos

![[#1] Capital Budgeting techniques | Payback Period Method | in Financial Management | by kauserwise®](https://img.youtube.com/vi/fbhUm8W-iLk/mqdefault.jpg)

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Definition of Payback Period

Chapter 1 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Payback Period (PBP)

- Definition: Time it takes to recover the initial investment.

Detailed Explanation

The Payback Period is a financial metric used to determine how long it will take for an investment to generate enough cash flow to recover the initial amount invested. It measures the amount of time it takes for a project to 'pay for itself.' This is particularly useful for businesses considering multiple investment opportunities, as it helps them find out which project will return their investment the quickest.

Examples & Analogies

Imagine you are running a small lemonade stand. If you spend $100 on equipment and supplies, and your stand makes $25 a week, the payback period would be 4 weeks (100 divided by 25). After 4 weeks, you would have recouped your initial investment.

Formula for Payback Period

Chapter 2 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Formula:

Initial Investment

Payback Period = Annual Cash Inflow

Detailed Explanation

The formula for calculating the Payback Period is straightforward. You divide the total initial investment by the annual cash inflow expected from the project. This gives you the number of years (or periods) it will take to recover the investment. This formula is an essential part of the decision-making process for businesses as they evaluate their investment options.

Examples & Analogies

Continuing with the lemonade stand example, if you invested $200 instead of $100, and your annual cash inflow is still $25 per week (or $1,300 per year), the payback period would now be 200 divided by 1,300, which is approximately 0.15 years (or about 8 weeks). This calculation shows how the payback period changes with different investment amounts and cash flows.

Advantages of Payback Period

Chapter 3 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

- Advantages:

- Simple and easy to understand.

- Good for assessing liquidity.

Detailed Explanation

One of the key advantages of the Payback Period method is its simplicity. It is easy to calculate and understand, making it a useful tool for managers who need to make quick decisions without delving into complicated calculations. Additionally, the Payback Period provides insights into liquidity, as it shows how quickly an investment can be recovered. This is especially important for businesses needing to maintain cash flow.

Examples & Analogies

Think of a small technology startup. If they are considering investing in software development, they can quickly use the Payback Period technique to determine how fast they can expect to see returns on their investment. By doing this analysis, they can confidently decide if the project will help meet their financial needs in the short term.

Disadvantages of Payback Period

Chapter 4 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

- Disadvantages:

- Ignores time value of money.

- Does not consider cash flows after payback period.

Detailed Explanation

Despite its benefits, the Payback Period has significant drawbacks. It does not take into account the time value of money, meaning it treats all cash inflows as equal regardless of when they occur. This can lead to misleading conclusions, especially for long-term projects. Additionally, the method ignores any cash flows that occur after the payback period, which may be critical for assessing the overall profitability of an investment.

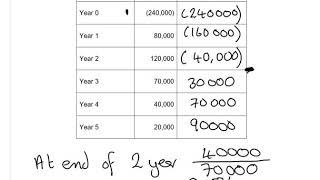

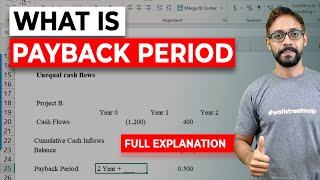

Examples & Analogies

Imagine two investments: Project A recoups its $1,000 investment in 2 years with cash flows of $500 each year. Project B also recoups $1,000, but in 4 years with $200 each year, followed by $1,500 the fifth year. The Payback Period would favor Project A despite Project B generating a much higher total cash inflow. This highlights how PBP can overlook the bigger picture of total returns.

Key Concepts

-

Payback Period: Measures time to recover the initial investment.

-

Annual Cash Inflow: Vital for calculating PBP.

-

Time Value of Money: Important to consider in investment evaluation.

Examples & Applications

An investment of $15,000 returns $5,000 annually. The PBP is 3 years.

A company invests $10,000 aiming for an annual return of $1,500. The PBP is approximately 6.67 years.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

Payback, payback, let’s not delay, cash flows come in, day by day.

Stories

Imagine a farmer who invests in seeds. He patiently waters and waits; three years later, he harvests enough crops to pay back what he spent!

Memory Tools

Remember PBP = Payback Recovery for brevity and clarity. Just think 'When am I back?'

Acronyms

PBP - 'Predicting Budgets Precisely.'

Flash Cards

Glossary

- Payback Period (PBP)

The time it takes to recover the initial investment from cash inflows.

- Initial Investment

The amount of money invested at the start of a project.

- Annual Cash Inflow

The cash received each year from an investment.

- Time Value of Money

The idea that money available now is worth more than the same amount in the future due to its potential earning capacity.

Reference links

Supplementary resources to enhance your learning experience.