Determinants of a Firm’s Supply Curve

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Technological Progress

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's discuss technological progress. Can anyone explain how advancements in technology might affect a firm's supply curve?

I think if a firm uses better technology, it can produce more with the same resources?

Exactly! This kind of progress usually lowers the marginal costs linked to production, right?

So, this means the supply curve shifts to the right?

Correct! This rightward shift means the firm will supply more at the same price. Can anyone recall what happens if the inputs become more efficient?

Yes! It results in a greater output for the same input levels.

Fantastic! So, technological advancements not only increase production efficiency but also lead to a greater supply at existing prices. Let's summarize this point: technological progress reduces costs and increases supply.

Input Prices

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Moving on, let's discuss input prices. Who can tell me how an increase in the price of an input affects the supply curve?

If the input prices like wages go up, production costs rise, right?

Absolutely! Higher production costs generally lead to a higher marginal cost, shifting the MC curve left. What does this imply for the supply curve?

The supply curve shifts left, meaning the firm will supply less at the same price?

Yes! Now what about decreases in input prices, can someone explain that effect?

Decreasing input prices would reduce production costs, allowing them to supply more at the same price, shifting the supply curve to the right.

Lovely! So let's summarize: increases in input prices decrease supply, while decreases in input prices increase it.

Impact of Unit Taxes

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now, let's talk about unit taxes. How do you think a government-imposed tax on each unit sold affects the supply curve?

Oh! If taxes are imposed per unit, it increases the cost to the firm, right?

Exactly! This raises both the average and marginal costs. Can you predict the supply curve's behavior in this case?

The supply curve will shift to the left, as the firm now supplies less at every price level?

Very well said! Would any of you like to provide a practical example of a unit tax affecting a firm?

For example, if the government taxed each soda sold, the company would supply fewer sodas due to increased costs from the tax.

Perfect example! So, to summarize: unit taxes increase costs and shift the supply curve left, reducing supply.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

The supply curve of a firm is influenced by factors like technological advancements that lower marginal costs and changes in input prices that can shift the supply curve left or right. Additionally, unit taxes can also affect the long-run supply curve.

Detailed

Determinants of a Firm’s Supply Curve

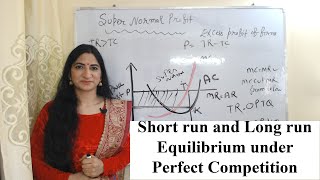

The supply curve of a firm reflects the quantity that it is willing to sell at different price levels, based on its production costs and other external factors. This section highlights the primary determinants that affect a firm's supply curve, specifically focusing on:

1. Technological Progress

Technological advancements can greatly enhance production efficiency. When a firm adopts new technologies, it can produce more output with the same amount of inputs or the same output with fewer inputs. This innovation typically reduces the firm's marginal cost at all levels of output, resulting in a rightward shift of the marginal cost (MC) curve and consequently the supply curve. This means that for any given market price, the firm is now able to supply a greater quantity of goods than before.

2. Input Prices

Changes in the prices of inputs have a direct impact on production costs. For instance, if the wage rate for labor increases, the cost of production rises. This increase typically results in a rise in the average cost of production and a leftward shift of the marginal cost curve, leading to a decrease in the quantity supplied at any given market price. Conversely, a fall in input prices would shift the supply curve to the right, allowing the firm to supply more at the same price levels.

3. Unit Taxes

Imposing a unit tax on each item sold raises the average cost for firms. The long-run supply curve shifts left as the firm alters its margins to account for the additional tax, which also limits the quantity supplied at every price level.

Understanding these determinants is crucial because they illustrate how responsive a firm's supply can be to various changes in internal and external factors.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Introduction to Determinants of Supply Curve

Chapter 1 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

In the previous section, we have seen that a firm’s supply curve is a part of its marginal cost curve. Thus, any factor that affects a firm’s marginal cost curve is of course a determinant of its supply curve.

Detailed Explanation

This chunk introduces the concept that the supply curve of a firm is directly related to its marginal cost curve. The marginal cost curve indicates how much it costs a firm to produce an additional unit of output. Therefore, any factor that causes the marginal cost to increase or decrease will also influence the firm's supply curve, shifting it to the left or right, respectively.

Examples & Analogies

Imagine that a bakery's supply of cookies is primarily influenced by the cost of flour. If the price of flour increases, the marginal cost of baking cookies rises, leading the bakery to supply fewer cookies at any given price. Conversely, if a new, cheaper supplier of flour is found, the bakery can produce more cookies at the same price.

Technological Progress

Chapter 2 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

4.5.1 Technological Progress Suppose a firm uses two factors of production – say, capital and labour – to produce a certain good. Subsequent to an organisational innovation by the firm, the same levels of capital and labour now produce more units of output.

Detailed Explanation

This chunk discusses how technological advancements can impact the supply curve. When a firm makes innovations that enhance its efficiency, such as using capital and labor more effectively, it can produce more with the same resources. As a result, the marginal costs decrease, effectively shifting the supply curve to the right, meaning that at any given price, the firm will supply more output.

Examples & Analogies

Consider a smartphone manufacturing company that implements a new software that automates part of its assembly line. With the same number of workers and machinery, the company can now produce 20% more smartphones by reducing the time required for assembly. This innovation effectively lowers the cost per smartphone, allowing the company to supply more at the same price.

Input Prices

Chapter 3 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

4.5.2 Input Prices A change in input prices also affects a firm’s supply curve. If the price of an input (say, the wage rate of labour) increases, the cost of production rises.

Detailed Explanation

Here, it is explained that fluctuations in the price of inputs, such as labor and materials, can lead to changes in a firm's supply curve. An increase in input prices raises production costs, which typically leads to an upward shift in the marginal cost curve. As costs increase, the firm’s supply curve shifts to the left, indicating that the firm will supply fewer products at each price level.

Examples & Analogies

Imagine a construction company that relies heavily on skilled labor. If local construction labor wages increase significantly due to high demand, the company struggles to maintain previous output levels without raising prices. The increased wage cost results in the company deciding to take on fewer projects or charge more for bids, reflecting a leftward shift in its supply curve.

Impact of a Unit Tax on Supply

Chapter 4 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

A unit tax is a tax that the government imposes per unit sale of output. For example, suppose that the unit tax imposed by the government is Rs 2.

Detailed Explanation

This part explains that when a unit tax is levied on products, the firm's cost of production rises correspondingly. Since the firm now must pay an additional cost for each unit produced, this results in an upward shift of both the long-run marginal and average cost curves. Consequently, the firm's long-run supply curve shifts to the left, indicating that at each price point, the firm will supply fewer goods than before the tax was imposed.

Examples & Analogies

For instance, if a soft drink manufacturer faces a new tax of Rs 2 per can, it adds this tax to its production costs. If the price per can remains the same but costs increase, the manufacturer may reduce the number of cans it is willing to supply, or increase the price if it wants to maintain profitability. Thus, the supply curve reflects less output available at each price level due to the tax burden.

Key Concepts

-

Technological Progress: A factor that lowers production costs and shifts the supply curve right.

-

Input Prices: Changes in production costs directly affect the supply curve position.

-

Unit Taxes: Taxes imposed per unit sold that shift the supply curve left, reducing quantity supplied.

Examples & Applications

In a scenario of technological advancement, a bakery that can produce ten loaves of bread per hour with old machinery may be able to produce twelve loaves using new technology, resulting in a rightward supply shift.

If the cost of flour increases significantly, the bakery may provide fewer loaves at each price level, shifting the supply curve to the left.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

A tech advancement, a great new way, lowers costs and helps goods sway.

Stories

Imagine a farmer using new irrigation technology that allows him to use less water and grow more crops; he can sell more at any price due to reduced costs.

Memory Tools

TIP - Technological Progress shifts right, Input prices shift left, Taxes shift left.

Acronyms

TIT - Technology Increases supply, Input Prices decrease it, Taxes do too.

Flash Cards

Glossary

- Supply Curve

A graphical representation that shows the relationship between the price of a good and the quantity supplied.

- Marginal Cost (MC)

The additional cost incurred by producing one more unit of a good.

- Technological Progress

Improvements in the processes used to produce goods, often enhancing efficiency.

- Input Prices

The costs associated with the resources needed to produce a good, including labor and materials.

- Unit Tax

A tax imposed by the government for each unit of good sold.

Reference links

Supplementary resources to enhance your learning experience.