Cost Accounting Basics – Types of Costs

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Understanding Cost Accounting

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Cost accounting is essential for internal business management. Unlike financial accounting, which focuses on external reporting, cost accounting provides detailed insights to managers. Can anyone tell me why this is crucial?

Maybe because it helps in making better decisions for the company?

Exactly! It assists in cost control and budgeting. We can remember this using the acronym CAP — Control, Ascertain, Plan. Who can explain one of these?

Control involves keeping costs within limits to maximize profitability.

Well done! Understanding these elements is fundamental in business. Let’s move on to different types of costs.

Types of Costs

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

We categorize costs based on various attributes. Starting with nature, could someone define direct costs?

Direct costs are those that can be directly traced to a specific product.

Right! Examples include raw materials and direct labor. What about indirect costs?

They’re costs that can’t be traced directly to a product, like utilities or rent.

Excellent! Remember this as DR & IR — Direct costs are Specific, Indirect are general. Let’s discuss the classification based on function next.

Cost Behavior

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now, let’s talk about how costs behave with production. Who can describe fixed costs?

Fixed costs don’t change with production levels, like salaries.

Correct! While variable costs do change with production, such as materials. Remember, FV — Fixed vs. Variable. Can anyone think of a mixed cost?

An electric bill can be mixed because it has a fixed charge and a variable usage charge.

Great example! Understanding these behaviors helps in making strategic pricing and production decisions.

Special Types of Costs

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let’s look at special types of costs. What is the opportunity cost?

It's the cost of what you give up when choosing one alternative.

Precisely! For example, if you choose to invest in a project instead of taking a job, what do we call the income lost from the job?

That would be the opportunity cost!

Excellent! What about a sunk cost?

That's a cost that has already been incurred and can't be recovered.

Exactly! We often make decisions based on future costs, not past ones. Always remember: Sunk is sunk!

Importance of Cost Classification

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Finally, why is it important to classify costs? What benefits can this provide?

It helps us with budgeting and making pricing decisions.

Exactly! It also assists in controlling costs and evaluating profitability. You can remember this with the acronym BPC — Budgeting, Pricing, Control. How does this impact a tech project, for instance?

In software projects, knowing fixed versus variable costs helps us in pricing SaaS models right.

Well said! Understanding these aspects directly influences success in tech and business!

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

Cost accounting is crucial for internal management, focusing on cost ascertainment, control, and profitability analysis. The section outlines several classifications of costs—based on nature, function, behavior, identifiability, and relevance—which provide essential insights into budgeting and financial planning.

Detailed

Cost Accounting Basics – Types of Costs

Cost accounting is pivotal for analyzing and managing an organization’s financial aspects. It helps in determining product and service costs, thus aiding in planning and decision-making.

Key Objectives of Cost Accounting

- Ascertainment of cost: Understanding total costs associated with products and services.

- Cost control: Strategies to maintain or reduce costs.

- Profitability analysis: Evaluating business profit margins.

- Inventory valuation: Determining the value of stock and assets.

- Budgeting & forecasting: Assisting in resource allocation and financial projections.

Classification of Costs

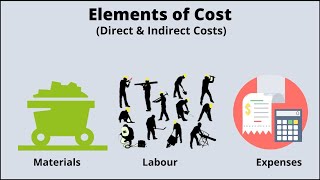

- Based on Nature/Elements:

- Direct Costs: Traceable to specific products or services (e.g., raw materials).

- Indirect Costs: Not directly linked to a single cost object (e.g., administrative expenses).

- Based on Function:

- Manufacturing Costs: Incurred in production processes.

- Administrative Costs: Related to overall management.

- Selling Costs: Expenses related to selling and distribution.

- Based on Behavior:

- Fixed Costs: Remain constant regardless of production levels (e.g., rent).

- Variable Costs: Change inversely with production volume (e.g., materials).

- Semi-variable Costs: Combination of fixed and variable components (e.g., electricity).

- Based on Identifiability:

- Traceable Costs: Directly associated with one cost object.

- Common Costs: Shared among multiple cost objects.

- Based on Relevance to Decision-Making:

- Relevant Costs: Future costs that differ with decisions.

- Irrelevant Costs: Costs that do not impact decision-making, such as sunk costs.

Special Types of Costs

- Opportunity Costs: Benefits lost from selecting one option over another.

- Sunk Costs: Costs already incurred with no recoverable value.

- Marginal Costs: Additional costs from producing one more unit.

- Controllable vs. Uncontrollable Costs: Managerial influence on costs matters.

- Imputed Costs: Hypothetical costs for asset utilization.

- Incremental & Differential Costs: Changes relevant to operational decisions.

Importance of Cost Classification

Cost classification supports budgeting, pricing decisions, cost control, and enhances profitability analysis, especially critical in tech-driven projects and startup environments. CSE students will find this knowledge invaluable for practical applications in software development and financial evaluation.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

What is Cost Accounting?

Chapter 1 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Cost accounting is the process of recording, classifying, analyzing, summarizing, and allocating costs associated with a process. Unlike financial accounting, which focuses on reporting to external stakeholders, cost accounting provides internal stakeholders with detailed cost information to aid in strategic decisions.

Objectives of Cost Accounting:

- Ascertainment of cost

- Cost control and cost reduction

- Profitability analysis

- Inventory valuation

- Assisting in budgeting and forecasting

Detailed Explanation

Cost accounting involves a systematic approach to capturing all costs related to a business process. It is distinct from financial accounting in its focus on internal decision-making rather than external reporting. The main objectives include determining costs accurately, controlling and reducing expenses, assessing profitability, valuing inventory properly, and supporting budgeting. These objectives empower managers to make informed strategic decisions.

Examples & Analogies

Imagine a chef at a restaurant who tracks every ingredient used in a dish down to the gram. By knowing exactly how much each ingredient costs, they can adjust their pricing or menu offerings effectively, ensuring that they remain profitable while serving delicious food.

Classification of Costs

Chapter 2 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Costs can be classified based on different attributes depending on the purpose. The most common types include:

20.2.1 Based on Nature/Elements

- Direct Costs: Costs that can be directly attributed to a specific product, service, or project.

- Examples: Raw materials, direct labor, specific software licenses.

- Indirect Costs (Overheads): Costs that cannot be directly traced to a single product or service.

- Examples: Office rent, general administration expenses, electricity for the whole office.

Detailed Explanation

Classification of costs helps in understanding how costs behave and their implications on financial planning. Direct costs can be linked directly to a specific output, such as materials or labor for a product. In contrast, indirect costs, also known as overheads, support a range of activities but don't tie directly to a specific product, making cost management more complex.

Examples & Analogies

Consider a toy manufacturer: the plastic used to create the toys is a direct cost because it can be traced back to each toy produced. On the other hand, the electricity used to run the machinery in the factory is an indirect cost, as it supports the production of all toys but cannot be assigned to any single toy.

Classification Based on Behavior

Chapter 3 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

20.2.3 Based on Behavior

These help in understanding how costs change with output:

- Fixed Costs:

- Do not change with output in the short term.

- Examples: Rent, salaries of permanent staff, depreciation.

- Variable Costs:

- Vary directly with the level of production.

- Examples: Raw materials, packaging.

- Semi-variable (Mixed) Costs:

- Contain both fixed and variable components.

- Example: Electricity bill (basic charge + usage-based cost).

Detailed Explanation

Understanding costs based on their behavior is crucial for budgeting and forecasting. Fixed costs remain constant regardless of production levels, while variable costs fluctuate directly with output. Semi-variable costs have elements of both and thus require careful management as production levels change. Recognizing these patterns can help managers prepare more effectively for financial planning.

Examples & Analogies

Think of a gym membership: the monthly fee is a fixed cost, while the number of towels used might represent a variable cost since it changes based on the number of clients. A semi-variable cost could be the electricity bill, which includes a fixed charge plus additional fees depending on usage for the gym's equipment.

Importance of Cost Classification

Chapter 4 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

20.4 Importance of Cost Classification

- Helps in Budgeting: Different costs affect budgets differently.

- Enables Pricing Decisions: Understanding variable and fixed costs is essential in setting prices.

- Improves Cost Control: Knowing which costs are controllable guides managerial action.

- Enhances Profitability Analysis: Distinguishing direct and indirect costs improves clarity on margins.

Detailed Explanation

Cost classification is vital for several reasons. It aids in creating realistic budgets by understanding how different types of costs behave. This knowledge allows businesses to set prices correctly based on a combination of fixed and variable costs. It also supports cost control by highlighting areas where managers can exert influence. Furthermore, clarity in cost distinctions improves profitability assessments, guiding strategic adjustments as necessary.

Examples & Analogies

Imagine a bakery planning a new dessert. By classifying costs, they can decide how much to charge; if they know the cost of ingredients (variable costs) and utility bills (fixed costs), they can price the dessert to ensure profit while remaining competitive.

Key Concepts

-

Cost Accounting: The process of recording and analyzing costs.

-

Direct Costs: Costs directly attributable to a product or service.

-

Indirect Costs: Costs not directly linked to a single product.

-

Fixed Costs: Remain constant regardless of production levels.

-

Variable Costs: Costs that change with production levels.

-

Opportunity Cost: The potential lost benefit from choosing one alternative over another.

-

Sunk Cost: Costs that have been incurred and cannot be recovered.

Examples & Applications

Direct costs include raw materials used in a product or wages paid to factory workers.

Indirect costs include office rent and utilities that cannot be traced to a specific product.

Fixed costs like monthly rent do not vary with production, while variable costs like material costs increase with output levels.

An opportunity cost is the income lost from not taking a job when starting a business.

Sunk costs could be the training expenses spent on an employee who leaves the company.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

Costs that are fixed stay high and dry, while variable costs dance and fly.

Stories

Imagine a baker who must pay a fixed rent for his shop (fixed costs) but buys more flour for each cake he bakes (variable costs). Every cake needs flour, but the rent stays the same, illustrating fixed and variable costs!

Memory Tools

To remember Direct vs Indirect Costs: 'D' for Direct, 'D' for Done - they're traceable like a line from point A to B. For Indirect Costs, think 'Indefinite'—they're harder to track!

Acronyms

Use the acronym IRM for Indirect, Relevant, Marginal costs which are often interrelated in analysis.

Flash Cards

Glossary

- Cost Accounting

The process of recording, classifying, analyzing, and summarizing costs to provide insight into business operations.

- Direct Costs

Costs that can be directly attributed to a specific product, service, or project.

- Indirect Costs

Costs that cannot be directly traced to a single product or service.

- Variable Costs

Costs that vary directly with production levels.

- Opportunity Cost

The potential benefit lost when one alternative is chosen over another.

- Sunk Cost

A cost that has already been incurred and cannot be recovered.

- Marginal Cost

The additional cost associated with producing one more unit of a product.

- Controllable Costs

Costs that can be influenced or controlled by a manager.

- Imputed Costs

Costs that are considered for decision-making but are not actually incurred.

- Incremental Costs

Additional costs resulting from a change in the level of activity.

- Differential Costs

The difference in costs between two alternatives.

Reference links

Supplementary resources to enhance your learning experience.