Production and Costs

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Introduction to Production

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Welcome everyone! Today, we're going to dive into the concept of production. Can anyone tell me what they think production means?

Isn't it about making goods or services?

Exactly! Production is the process where inputs are transformed into outputs. For example, a tailor uses cloth and a sewing machine to produce shirts. This transformation is crucial in the economy.

So, inputs can be anything from materials to labor, right?

That's correct! Inputs include labor, machines, and land. Remember the acronym LML for Labor, Machines, and Land to recall these inputs. Let's summarize our main points: Production involves turning various inputs into usable products or services, and these inputs can be diverse.

Understanding Costs of Production

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's talk about the costs of production. What do you think this means?

Does it refer to the money firms spend on buying inputs?

Yes! The cost of production includes what firms pay for their inputs—labor, materials, and so on. This is crucial because it affects their profit. Can anyone explain why knowing these costs is important?

If they know their costs, they can figure out how much they need to sell to cover those costs and make a profit!

Exactly! And do you all remember how to calculate profit? It's the revenue minus the cost of production. Let's create a simple sentence to remember: Profit = Revenue - Costs. Great work!

Relationship Between Inputs and Outputs

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now we need to understand how inputs relate to output. Why do you think it's essential to analyze this relationship?

To maximize profits? If firms know the best combination of inputs, they can produce the most output, right?

Correct! Identifying the most efficient use of inputs to create outputs at the maximum profit is crucial for any firm. Let's create a mnemonic to remember this: 'P.O.O'—Profit Optimized Output! Perfect!

That makes sense. So the best conditions for maximizing profit relies on optimizing the input use?

Exactly! Summing up today’s discussion: We looked at how the relationship between inputs and outputs is key for profit maximization.

Immediate Production Assumption

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's take a moment to address a simplifying assumption we made earlier: that production happens instantly. What does this mean?

It means we’re not considering the time it takes to make something?

Right! We’re simplifying to focus on the transformation process without the time element. This helps us learn the core concepts without getting bogged down in details. Remember that sometimes simplifying assumptions are used to clarify a model.

Are there any real-life examples where production isn't instantaneous?

Absolutely! Think about baking a cake—there's preparation time involved. Let’s summarize: We discussed how assuming instantaneous production helps us focus on fundamental concepts, but it's essential to recognize it isn't always the case.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

In this section, we explore the process of production, the costs incurred by firms in acquiring inputs, and the relationship between inputs and outputs, leading to profit maximization. Practical examples illustrate the diverse operations of different producers.

Detailed

Detailed Summary

In this chapter, we focus on the behavior of producers within the economy. Production is defined as the transformation of various inputs such as labor, machines, and raw materials into finished products or services. Producers, commonly referred to as firms, utilize these inputs to create outputs that are either consumed directly by consumers or used for further production by other firms.

Key Points Explained:

- Definition of Production: Production involves the combination of inputs—like labor, machines, land, and raw materials—to create outputs. For instance, a tailor uses a sewing machine and cloth to make shirts, while a farmer uses land and fertilizers to grow crops.

- Instantaneous Production: This section makes certain simplifying assumptions about the production process, stating that production occurs instantaneously in this context, emphasizing the immediate transformation of inputs into outputs.

- Costs of Production: Firms incur costs for the inputs they require. This cost is fundamental to understanding the overall profitability of a firm, as it directly impacts the revenue earned once the products are sold.

- Revenue and Profit: The income generated from selling produced goods minus the cost of production yields profit. The ultimate goal of firms is to maximize this profit.

- Next Steps: The subsequent discussions will delve deeper into the relationship between inputs and outputs and explore the firm's cost structure to identify levels of output where profit maximization occurs.

Overall, this section sets the foundation for understanding producer behavior in the economy.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Introduction to Production

Chapter 1 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

In the previous chapter, we have discussed the behaviour of the consumers. In this chapter as well as in the next, we shall examine the behaviour of a producer. Production is the process by which inputs are transformed into ‘output’. Production is carried out by producers or firms. A firm acquires different inputs like labour, machines, land, raw materials etc. It uses these inputs to produce output. This output can be consumed by consumers, or used by other firms for further production.

Detailed Explanation

Production is the process where various inputs, such as labor and materials, are combined to create goods or services. Producers or firms are responsible for this transformation, providing necessary resources like machines and labor to manufacture the final product. For example, a farmer uses land and seeds to grow crops, while a factory uses machines and labor to build cars.

Examples & Analogies

Think of production as baking a cake. You need ingredients (inputs) like flour, eggs, and sugar, which you combine to create a delicious cake (output). Just like a baker gathers and mixes the right ingredients, a producer must assemble the right resources to make a product.

Cost of Production

Chapter 2 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

In order to acquire inputs a firm has to pay for them. This is called the cost of production. Once output has been produced, the firm sells it in the market and earns revenue. The difference between the revenue and cost is called the firm’s profit. We assume that the objective of a firm is to earn the maximum profit that it can.

Detailed Explanation

The cost of production includes all expenses a firm incurs to gather inputs, manufacture goods, and bring them to market. Once they sell the finished product, they earn revenue. The profit is simply the difference between how much they make from selling their goods and what they spent on making them. Firms aim to maximize profits by keeping costs low and selling at higher prices.

Examples & Analogies

Imagine a lemonade stand. If you spend $5 on lemons and sugar (cost of production) and sell lemonade for $10 (revenue), your profit is $5. Your goal is to sell as much lemonade as possible while keeping costs down to maximize that profit.

Production Function

Chapter 3 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

The production function of a firm is a relationship between inputs used and output produced by the firm. For various quantities of inputs used, it gives the maximum quantity of output that can be produced. The production function tells us the maximum amount of wheat he can produce for a given amount of land that he uses, and a given number of hours of labour that he performs.

Detailed Explanation

The production function describes how different quantities of inputs contribute to the output a firm can produce. It shows the maximum output achievable with specific combinations of inputs, like the amount of labor and land a farmer uses. If a farmer uses two hours of labor and one hectare of land, they might be able to maximize production to two tonnes of wheat.

Examples & Analogies

Consider the production function as a recipe. For instance, a recipe that calls for 2 cups of flour and 1 cup of sugar is designed to make a specific number of cookies. If you change the amounts of the ingredients, you might get more or fewer cookies, just like varying labor and land will yield different amounts of wheat.

Isoquants

Chapter 4 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

An isoquant is the set of all possible combinations of the two inputs that yield the same maximum possible level of output. Each isoquant represents a particular level of output and is labeled with that amount of output.

Detailed Explanation

Isoquants help visualize how different combinations of inputs can produce the same output level. For example, if a farmer can grow 10 units of wheat by using 4 units of labor and 1 unit of capital or by using other combinations, these would all lie on the same isoquant line, indicating they yield the same output.

Examples & Analogies

Think of isoquants like different routes to the same destination. You can get to a friend's house using various paths while still arriving at the same time; similarly, you can produce the same output using different combinations of inputs.

Short Run vs Long Run

Chapter 5 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

In the short run, at least one of the factor – labour or capital – cannot be varied, and therefore, remains fixed. In the long run, all factors of production can be varied.

Detailed Explanation

The key difference between the short run and the long run in production is flexibility. In the short run, some factors (like machinery) can't be changed, so firms must work with what they have to adjust output. In contrast, in the long run, firms can modify all inputs to achieve desired output levels.

Examples & Analogies

Imagine you're hosting a party (the short run). You can rearrange the furniture or buy more snacks, but you can't change the size of your house. In the long run, if you decide to renovate your home, you can expand and change everything to better accommodate parties.

Total Product, Average Product, and Marginal Product

Chapter 6 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Total Product (TP) is the output produced by varying one input while keeping others constant. Average Product (AP) is the output per unit of variable input (TP divided by the amount of input used), while Marginal Product (MP) is the change in output resulting from a one-unit change in the input.

Detailed Explanation

Total Product measures the overall output produced for certain input levels; Average Product gives a sense of productivity per unit of input, and Marginal Product indicates how much additional output is gained from using one more unit of that input. Understanding these concepts helps firms optimize their production processes.

Examples & Analogies

Think about a pizza shop. Total Product is the number of pizzas made in a day. Average Product is the number of pizzas each worker makes on average. Marginal Product tells the shop owner how many additional pizzas can be created if they hire one more worker.

Law of Diminishing Marginal Product

Chapter 7 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

The law of variable proportions states that, as one input is increased while others are held constant, the marginal product of that input will eventually decrease after a certain point.

Detailed Explanation

Initially, as a firm adds more of a variable input (like labor), output increases significantly. However, after reaching an optimal point, adding more input results in smaller increases in output because resources may become too crowded or inefficiently used. This is the law of diminishing marginal product.

Examples & Analogies

Think about planting seeds in a garden. In the beginning, adding more seeds leads to more flowers. However, after a while, if you overcrowd the garden with too many seeds, they compete for sunlight and nutrients, and not all of them will flourish.

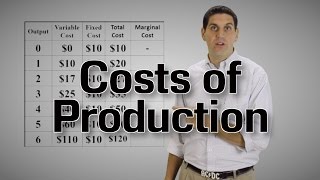

Short Run and Long Run Costs

Chapter 8 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

In the short run, firms face total fixed costs that do not change with output levels, while in the long run, all costs are variable. Total cost is the sum of total fixed and total variable costs.

Detailed Explanation

In the short run, businesses have fixed costs that must be paid regardless of output, like rent or salaries. Total Variable Costs rise as production increases since these costs fluctuate with output. Long run measures take all costs into account, allowing businesses more flexibility to adapt to outputs and change inputs without fixed costs.

Examples & Analogies

Imagine renting an apartment (short run). You pay the same rent every month regardless of how many rooms you use. In the long run, if you decide to buy a house instead, you could later decide to sell or renovate to increase your space and utility.

Key Concepts

-

Production: The process of transforming inputs into outputs.

-

Inputs: Resources used by producers in the production process.

-

Costs of Production: The expenses incurred in acquiring those inputs.

-

Revenue: The income generated from selling outputs.

-

Profit: The difference between revenue and costs, representing the financial gain.

Examples & Applications

A tailor producing shirts using cloth, thread, and a sewing machine.

A farmer cultivating wheat using land, labor, and fertilizers.

A car manufacturer using steel and machinery to assemble cars.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

In the world of production, inputs play a role;

Stories

Once upon a time in a bustling town, there was a tailor who made fashionable gowns. He had cloth, a sewing machine, and skill in his hands. With inputs combined, he answered demands.

Memory Tools

Remember LML for Labor, Machines, and Land as inputs for production!

Acronyms

P.O.O — Profit Optimized Output helps us recall the concept of maximizing profits through efficient production.

Flash Cards

Glossary

- Production

The process of transforming inputs like labor and raw materials into outputs, such as goods and services.

- Inputs

The resources utilized by firms to produce goods or services, including labor, machinery, land, and raw materials.

- Costs of Production

Expenses incurred by firms to acquire inputs necessary for producing outputs.

- Revenue

The total income generated from selling produced goods or services.

- Profit

The difference between total revenue and total cost; the financial gain achieved by firms.

Reference links

Supplementary resources to enhance your learning experience.