Short Run Costs

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Total Fixed Cost and Total Variable Cost

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we're going to start by defining total fixed costs (TFC) and total variable costs (TVC). Can anyone tell me what they understand by fixed costs?

I think fixed costs are expenses that don’t change regardless of how much you produce.

Exactly! TFC remains constant no matter the level of output. Now, how about variable costs?

Variable costs change based on the production level. So, if we produce more, we'll pay more.

Correct! Remember, the sum of TFC and TVC gives us the total cost of production. Can anyone summarize why understanding these costs is vital for a firm?

Knowing these costs helps a firm decide how to price its products and manage expenses.

That's a great insight! Understanding your cost structure is key for production planning and profitability.

Calculating Total Costs

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now that we understand fixed and variable costs, let's delve into total costs. Who can tell me how total costs are calculated?

Total cost is the sum of total fixed cost and total variable cost, right?

Exactly! The formula is TC = TFC + TVC. Let's say TFC is Rs 20 and TVC is Rs 30. What is the total cost?

That would be Rs 50.

Great! Now, how would you calculate the average cost per unit?

We divide total cost by the number of units produced, right?

Correct! You can remember this using the acronym ATC for Average Total Cost. Understand how mastering these calculations can help in pricing strategies?

Yes! It shows how much to charge to cover costs.

That's right! Good job, everyone!

Understanding Marginal Costs

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's transition to discussing short run marginal cost (SMC). What does SMC represent?

SMC shows the additional cost incurred by producing one more unit of output.

Exactly! And as you increase production, how does this impact total variable cost?

Total variable cost increases as output rises.

Correct! Can anyone identify how SMC relates to AVC and SAC curves?

I think SMC intersects AVC at its minimum point.

Great! That’s an important relationship in maximizing profit. Remember: when SMC is less than AVC, AVC decreases.

And when SMC is greater than AVC, it rises!

Exactly! Very well done!

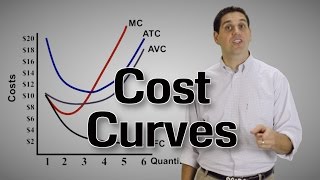

Shapes of Cost Curves

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now, let’s visualize the shapes of the cost curves. Why do you think the average cost curves are commonly U-shaped?

Because initially, costs decrease as production increases, then increase after a certain point of output.

Exactly, and this is due to the law of diminishing returns in the short run. Can anyone summarize this law for us?

The marginal product of a factor will eventually decrease as we increase the variable input while keeping other inputs constant.

Well put! This principle is key in understanding why cost curves behave the way they do. In essence, the shape guides firms in their production levels and cost management strategies.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

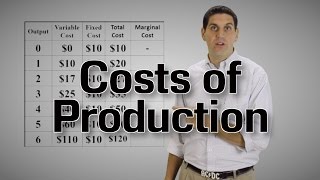

In this section, we explore short run costs, defining key concepts such as total fixed cost (TFC), total variable cost (TVC), and total cost (TC). We also examine average cost calculations, including average fixed cost (AFC), average variable cost (AVC), and the significance of short run marginal cost (SMC) in relation to production output.

Detailed

Short Run Costs

In the short run, certain factors of production remain fixed, impacting the cost structure for firms. The costs involved in production can be categorized into:

- Total Fixed Cost (TFC): These are the costs that do not change regardless of the quantity of output produced. For instance, a factory's rent is a fixed cost.

- Total Variable Cost (TVC): Unlike fixed costs, variable costs change with the level of output. As a firm increases production, it incurs higher variable costs due to the need for additional materials or labor.

- Total Cost (TC): This is the sum of TFC and TVC, representing the total expenditure a firm incurs in order to reach a certain level of production.

The relationships among TFC, TVC, and TC are established through the equation: TC = TFC + TVC.

In addition to these costs, firms must also consider average costs (per unit). The short run average cost (SAC) is calculated as:

- Average Total Cost (ATC) = TC / quantity produced

- Average Variable Cost (AVC) = TVC / quantity produced

- Average Fixed Cost (AFC) = TFC / quantity produced

The short run marginal cost (SMC) is another critical aspect that measures the change in total cost generated by producing one additional unit of output and is defined as:

- SMC = Change in TC / Change in Output

As output rises, TVC and TC generally increase, whereas TFC remains constant. This section also indicates the ‘U’-shaped nature of cost curves pertinent to SAC, AVC, and SMC, highlighting their implications in cost management and pricing strategies as firms optimize their production in the short run.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Understanding Short Run Costs

Chapter 1 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

We have previously discussed the short run and the long run. In the short run, some of the factors of production cannot be varied, and therefore, remain fixed. The cost that a firm incurs to employ these fixed inputs is called the total fixed cost (TFC).

Detailed Explanation

In economics, we distinguish between short run and long run based on the flexibility of inputs. In the short run, certain inputs, like machinery or land, are fixed, meaning their quantities cannot be changed. The costs associated with these fixed inputs are referred to as Total Fixed Costs (TFC). For example, if a factory has to pay rent on its building, that's a fixed cost that does not change with the level of output. So, no matter how many products the factory makes, it must pay the same amount of rent each month.

Examples & Analogies

Think of a pizza restaurant. If the restaurant rents its space for $1,000 a month, that is a fixed cost. Whether the restaurant sells 10 pizzas or 100 pizzas, the rent remains the same.

Variable Costs in the Short Run

Chapter 2 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

To produce any required level of output, the firm, in the short run, can adjust only variable inputs. Accordingly, the cost that a firm incurs to employ these variable inputs is called the total variable cost (TVC).

Detailed Explanation

In contrast to fixed costs, variable costs can change depending on the level of output. These costs are associated with the inputs that can be adjusted, such as labor or raw materials. The more output produced, the higher the Total Variable Cost (TVC). For instance, if the pizza restaurant decides to hire more chefs to handle a rush of orders, the wages for the additional chefs reflect a variable cost. The TVC increases with the scale of production.

Examples & Analogies

Imagine the same pizza restaurant needs to buy more ingredients, like cheese and flour, when it decides to make more pizzas. The costs for these ingredients increase as production scales up, representing variable costs.

Total Cost Computation

Chapter 3 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Adding the fixed and the variable costs, we get the total cost (TC) of a firm

TC = TVC + TFC.

Detailed Explanation

The overall cost of production for a firm is calculated by combining both total fixed costs and total variable costs into what we call total costs (TC). This equation, TC = TVC + TFC, captures the complete financial picture of production. The total costs provide insight into how much it costs to produce a given level of output. An understanding of total cost is crucial for firms as they aim to maximize profit by balancing costs and revenues.

Examples & Analogies

For our pizza restaurant, if the fixed cost is the monthly rent of $1,000, and the variable costs increase based on the number of pizzas made (say, $500 for ingredients and wages when making 100 pizzas), the total cost would be $1,500. This helps the restaurant owner decide how many pizzas to sell to make a profit.

Average and Marginal Costs: Key Definitions

Chapter 4 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

The short run average cost (SAC) incurred by the firm is defined as the total cost per unit of output. We calculate it as

SAC = TC / q.

Detailed Explanation

Average costs are important in determining efficiency in production. The short run average cost (SAC) is calculated by dividing total cost (TC) by the quantity of output (q). This provides an insight into how much it costs the firm to produce each individual unit of output, which is essential for pricing and profit strategies. Lower SAC can indicate efficiency, while higher costs per unit might necessitate adjustments in operations or pricing.

Examples & Analogies

Using the pizza restaurant example, if the total cost of producing 100 pizzas is $1,500, then the average cost per pizza would be $15. This helps to set the selling price of each pizza to ensure profit margins.

Understanding Marginal Costs

Chapter 5 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

The short run marginal cost (SMC) is defined as the change in total cost per unit of change in output

SMC = change in total cost / change in output.

Detailed Explanation

The marginal cost is crucial for understanding the cost implications of increasing production. It represents the additional cost incurred from producing one more unit of output. If a firm knows its marginal costs, it can make informed decisions about whether to increase production based on profitability. SMC is calculated by observing the change in total cost that arises from a one-unit increase in output, highlighting the cost impact of scaling production up or down.

Examples & Analogies

Returning to our pizza restaurant, if increasing production from 100 pizzas to 101 pizzas causes the total cost to rise from $1,500 to $1,515, the marginal cost of making that additional pizza is $15. This calculation helps ensure that the price set for each pizza covers the marginal cost, allowing the firm to remain profitable.

Key Concepts

-

Total Fixed Cost (TFC): Costs that do not vary with production levels.

-

Total Variable Cost (TVC): Costs that change as production levels change.

-

Total Cost (TC): The total cost incurred, which is the sum of TFC and TVC.

-

Short Run Marginal Cost (SMC): The additional cost of producing one more unit of output.

-

Average Cost (AC): The cost per unit produced based on total costs.

-

Average Variable Cost (AVC) and Average Fixed Cost (AFC): Costs per unit based on variable and fixed components, respectively.

Examples & Applications

If a firm has a fixed cost of Rs 50 and a variable cost of Rs 20 when producing 2 units, the total cost would be Rs 70.

If the company produces 5 units, and the variable cost for those units is Rs 100, and fixed costs remain at Rs 50, then TC = 50 + 100 = Rs 150.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

In the short run, fixed costs stay, as variable costs rise when output plays.

Stories

Imagine a baker who pays the same rent for a store; no matter how many loaves, the rent is twenty-five, forevermore. But for flour, eggs, and sugar, the more he bakes, the more these costs suddenly take!

Memory Tools

Fried Vegetables Can always be Costly - to remember: Fixed, Variable, Cost (TFC, TVC, TC).

Acronyms

AVC - Average Variable Cost; think about it as dividing total variable costs by output.

Flash Cards

Glossary

- Total Fixed Cost (TFC)

The costs that do not change, regardless of the output level produced.

- Total Variable Cost (TVC)

The costs that vary with the level of output produced.

- Total Cost (TC)

The sum of total fixed cost and total variable cost.

- Short Run Marginal Cost (SMC)

The change in total cost that arises from producing one additional unit of output.

- Average Cost (AC)

The total cost divided by the quantity of output produced.

- Average Variable Cost (AVC)

The total variable cost divided by the quantity of output produced.

- Average Fixed Cost (AFC)

The total fixed cost divided by the quantity of output produced.

Reference links

Supplementary resources to enhance your learning experience.