Main Features - 2.3.2

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Definition of Capitalist Economy

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today we are discussing the capitalist economy. Can anyone tell me what a capitalist economy is?

Is it where everything is owned by private people?

Exactly! A capitalist economy is defined as one where the means of production are owned and controlled by private individuals. This ownership leads to a focus on profit. We can remember this with the acronym 'PROFIT', which stands for Private ownership, Resources Controlled by individuals, Optimization for profit, Freedom of choice, and Institutional market forces.

So, does that mean the government doesn't get involved much?

Correct! There is minimal government interference, allowing for a free market to operate. The dynamic nature of this economy is truly fascinating!

Can you give us an example of a capitalist economy?

Sure! The United States is a prime example of a capitalist economy. It features strong private ownership and minimal government regulation.

To summarize, a capitalist economy features private ownership, limited government intervention, and a profit motive.

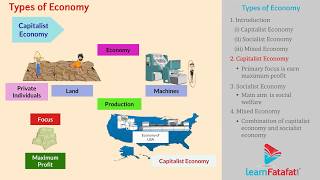

Main Features of a Capitalist Economy

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let’s dive deeper into the main features of capitalist economies. Can anyone name one of these features?

There’s the profit motive, right?

Exactly! The profit motive is central to capitalism. It's what drives individuals and businesses to work hard and innovate. The acronym 'FREEDOM' where F stands for Freedom of Choice, R for Resources owned by individuals, E for Economic profit, E for Entrepreneurship, D for Demand-Supply balance, and O for Ownership can help you remember this!

What about prices? How are they determined in a capitalist economy?

Great question! Prices in a capitalist economy are determined purely by market forces, specifically supply and demand. So, when demand is high and supply is low, prices tend to rise.

That makes sense! Are there any downsides to a capitalist economy?

Definitely! While capitalism fosters innovation and efficiency, it can also lead to inequality as wealth accumulates in the hands of a few. But remember, each economy has its pros and cons!

In summary, the main features of capitalist economies include private ownership, minimal government intervention, the profit motive, and market-driven prices.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

Capitalist economies are defined by private ownership and the absence of government interference. Key features include the profit motive, freedom of choice, and price determination by market forces. Examples of capitalist economies are the United States, Japan, and Australia.

Detailed

Main Features of a Capitalist Economy

In a capitalist economy, the primary distinguishing feature is the private ownership of resources and property by individuals or businesses. This ownership structure drives the profit motive, encouraging entrepreneurs and companies to innovate and optimize efficiency to maximize profits. Consequently, stakeholders rely on the freedom of choice to engage in commerce without significant government constraints, allowing for a dynamic marketplace where consumers ultimately dictate the demand for products and services.

Market forces, specifically supply and demand, play a crucial role in determining prices, ensuring that prices reflect the subjective value consumers place on goods and services. As such, government interference remains minimal, preserving a competitive environment that theoretically leads to the most efficient allocation of resources.

Some prominent examples of capitalist economies include the United States, Australia, and Japan. These nations exemplify varying degrees of capitalism, showcasing the adaptability of the capitalist model across different cultural and economic contexts.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Private Ownership of Property and Resources

Chapter 1 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

● Private ownership of property and resources

Detailed Explanation

In a capitalist economy, the means of production—such as factories, machinery, and land—are owned by private individuals or businesses. This means that individuals have the right to buy, sell, and manage these resources as they see fit. This private ownership allows people to control their own economic resources, leading to competition and innovation.

Examples & Analogies

Think of a local bakery owned by a baker. The baker buys the ingredients, rents the space, and decides what types of bread to sell. Because they own the bakery, they can respond to customer preferences quickly and make changes to their offerings without needing permission from a government authority.

Freedom of Choice and Enterprise

Chapter 2 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

● Freedom of choice and enterprise

Detailed Explanation

Capitalist economies grant individuals and businesses the freedom to make their own economic choices. This includes what to produce, how to produce it, and how to sell it. Entrepreneurs can start new businesses based on their observations of market needs, and consumers can choose from a wide range of products and services offered by these businesses.

Examples & Analogies

Consider the technology market where an entrepreneur notices that people are looking for more user-friendly smart home devices. They decide to create and sell a new device. This entrepreneurial spirit drives innovation, as anyone can enter the market with a new idea.

Profit Motive

Chapter 3 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

● Profit motive is the driving force

Detailed Explanation

In a capitalist economy, the primary incentive for individuals and companies to produce goods and services is the profit they can earn. This profit motive encourages efficiency, innovation, and risk-taking, as businesses strive to maximize their profits by meeting consumer demands effectively.

Examples & Analogies

Think of a smartphone manufacturer. If they can create a better phone that consumers love, they will sell more and earn higher profits. This drive for profit pushes them to invest in research and development, improving technology and customer satisfaction.

Minimal Government Interference

Chapter 4 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

● Minimal government interference

Detailed Explanation

A key characteristic of a capitalist economy is that there is little government intervention in business operations and market conditions. The government's role is primarily to maintain law and order and protect property rights, allowing the free market to dictate the prices and production of goods based on supply and demand.

Examples & Analogies

Imagine a farmer who grows vegetables. In a capitalist system, as long as they comply with health and safety standards, they can choose whether to sell directly to consumers, at a market, or to grocery stores without needing government approval for each decision.

Prices Determined by Market Forces

Chapter 5 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

● Prices determined by market forces (demand and supply)

Detailed Explanation

In capitalist economies, prices of goods and services are established by the interaction of supply and demand. When demand for a product increases and supply remains constant, prices tend to rise. Conversely, if supply exceeds demand, prices typically fall. This self-regulating nature of the market helps allocate resources efficiently.

Examples & Analogies

For example, during a drought, the supply of water may decrease. As people still need water, the demand remains high while the supply drops, leading to higher prices for bottled water in stores. Businesses respond by sourcing alternative supplies or offering promotions on less popular products.

Key Concepts

-

Private Ownership: Refers to the control of production resources by individuals.

-

Minimal Government Interference: Suggests a limited role of the government in economic activities.

-

Profit Motive: A central feature driving individuals and businesses to pursue financial gain.

-

Market Forces: Prices are influenced by supply and demand dynamics.

Examples & Applications

The United States exemplifies a capitalist economy with its focus on private enterprise and market-driven price determination.

Japan showcases an advanced capitalist economy that combines technology and innovative practices to benefit consumers.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

In a capitalist zone, prices are flown, private’s the tone, let profits be known.

Stories

Imagine a farmer who sells apples. His prices go up when people want more apples, showing how demand influences costs—all without government setting prices.

Memory Tools

Remember 'P.M.M.P.': Private ownership, Market forces, Minimal interference, Profit motive.

Acronyms

C for capitalism

Choice

Competition

Control by private.

Flash Cards

Glossary

- Capitalist Economy

An economy where the means of production are owned and controlled by private individuals, driving profit maximization.

- Profit Motive

The primary incentive in a capitalist economy that encourages individuals and businesses to maximize their financial gain.

- Market Forces

Economic factors that affect the supply and demand of goods and services, determining their prices.

Reference links

Supplementary resources to enhance your learning experience.