Format of a Journal

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Understanding Journal Entry Components

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today we will learn about the format of a journal entry. Can anyone tell me what a journal is in accounting?

Is it where we write down all the financial transactions?

Exactly! The journal is the primary book of entry. Now, let’s look at the different components. Can anyone name one?

The date when the transaction happened?

Right! The date is essential. We record transactions chronologically to keep track of them easily.

What else do we write in the journal?

Great question! We also have particulars, which include the accounts involved and a brief narration of the transaction.

What about the amounts?

Good point! Finally, we have the debit and credit amounts. It’s crucial that they match according to the double-entry system. Remember: every debit has a corresponding credit!

So let's recap: A journal entry includes the date, particulars, and the debit and credit amounts. Any questions before moving on?

The Structure of a Journal Entry

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now, let’s look at how a journal entry is structured. Can someone read out the format I just wrote on the board?

Sure! We have the date, then particulars, followed by L.F., and finally debit and credit amounts.

Correct! The L.F. is important as it connects the journal to the ledger. Why do you think knowing where to find these accounts is beneficial?

So we can quickly verify or update the Ledger?

Exactly! The L.F. helps maintain organization and ensures efficient tracking. Now, let’s see an example of a journal entry.

"If we sold goods for cash worth ₹5,000 on July 1, 2025, it will look like this:

Practice Journal Entries

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now that we understand the format, let’s practice creating our journal entries. I'll give you some transactions, and you’ll record them in your journals. Ready?

Yes! What’s the first transaction?

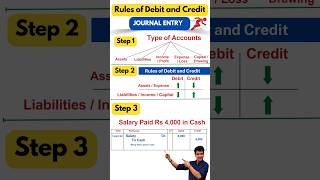

Great! Transaction one: On July 5, 2025, purchased office supplies for ₹2,000 cash. Can anyone tell me how they would record that?

I would write `05/07/2025 Office Supplies A/c Dr. 2,000 To Cash A/c 2,000`.

Perfect! You’re getting the hang of it. The office supplies inventory increases; thus, it's a debit. Cash decreases, so it’s a credit.

What if it was on credit instead?

Fantastic question! In that case, you'd debit Office Supplies and credit Accounts Payable instead. Remember, it changes the cash flow! Now, let’s review a final example.

Any last questions before we wrap up?

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

In this section, the format of a journal entry is outlined, highlighting its key components such as date, particulars, ledger folio, and the amounts for debit and credit. Understanding this format is essential for practicing accurate record-keeping in accounting.

Detailed

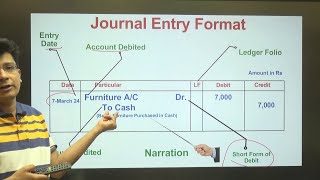

Format of a Journal

The journal serves as the primary book of accounting entry, where transactions are first recorded in a chronological order. Each journal entry contains several key components:

- Date: This indicates when the transaction occurred.

- Particulars: Accounts involved along with a narration explaining the transaction.

- L.F. (Ledger Folio): The page number where the corresponding ledger account can be found.

- Debit and Credit: The amounts that signify the financial impact of the transaction according to the double-entry accounting system.

Example Journal Entry

The format can be illustrated as follows:

Date Particulars L.F. Debit (₹) Credit (₹) 01/07/2025 Cash A/c 101 5,000 5,000 Dr. To Sales A/c (Goods sold for cash)

This layout ensures clear communication within accounting practices, providing a systematic approach to recording financial transactions.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Overall Structure of a Journal Entry

Chapter 1 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Date Particulars L.F. Debit (₹) Credit (₹)

01/07/2025 Cash A/c 101 5,000 5,000

Dr. To Sales A/c (Goods sold for cash)

Detailed Explanation

The format of a journal entry is crucial for maintaining organized records. Each entry contains several components:

1. Date: The specific day the transaction took place.

2. Particulars: The names of the accounts involved along with a brief description of the transaction. Here, 'Cash A/c' and 'Sales A/c' are the accounts affected.

3. L.F. (Ledger Folio): Refers to the page number in the ledger where this transaction is recorded, facilitating easy access for future reference.

4. Debit and Credit Columns: The amounts involved in the transaction, divided into debits (left side) and credits (right side). This structure follows the double-entry accounting system, where every debit must have a corresponding credit.

Examples & Analogies

Think of a journal entry like a detailed receipt from a purchase. When you buy something, the receipt has the date of the purchase, what you bought (the particulars), and the total amount paid (which aligns with debits and credits). Just like you can refer back to your receipt for details, the journal helps accountants trace back every financial transaction.

Components of a Journal Entry Explained

Chapter 2 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Explanation:

- Date: When the transaction occurred

- Particulars: Accounts involved and narration

- L.F.: Page number of ledger

- Debit & Credit: Amounts recorded as per the double-entry system

Detailed Explanation

Let's break down the components of a journal entry:

1. Date: This is essential for chronological sorting. Knowing when a transaction occurred helps in organizing financial statements over time.

2. Particulars: This section identifies the 'who and what' of the transaction. For example, in our previous example, it explains that cash was received from sales.

3. L.F.: This is like a bookmarks in a book. It tells you where to look in the ledger for that specific transaction.

4. Debit & Credit: This part reflects the accounting principle where each debit entry must be matched with a credit entry to keep the books balanced.

Examples & Analogies

Imagine you are writing in a diary. Each entry has a date, what happened (the particulars), and sometimes you might use shorthand symbols or codes to quickly reference where to find more details (like L.F.). And just like balancing your emotional state by writing down positive and negative experiences, in accounting, every transaction needs balance through debits and credits.

Key Concepts

-

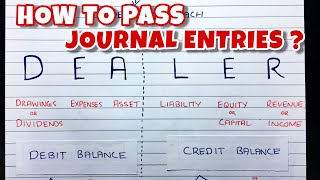

Journal: The primary book where all transactions are first recorded.

-

Journal Entry: An individual transaction record, consisting of several components.

-

Date: The date a transaction occurs, crucial for chronological order.

-

Particulars: The accounts involved in a transaction and accompanying explanation.

-

Debit and Credit: Reflects the corresponding effects on accounts as per the double-entry system.

Examples & Applications

Journal Entry Example: 01/07/2025 Cash A/c Dr. 5,000 To Sales A/c 5,000

If you purchased office supplies for ₹2,000 cash, the entry would be: 05/07/2025 Office Supplies A/c Dr. 2,000 To Cash A/c 2,000

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

Date and particulars, keep them neat, Debit and credit, make it complete!

Stories

Imagine a cashier writing down each sale in a diary. Each entry starts with the date, followed by who bought what, and how much was paid. This could be your journal!

Memory Tools

D-P-L-D-C: Date, Particulars, L.F., Debit, Credit - remember the order for a perfect journal entry!

Acronyms

JPDC

Journal

Particulars

Date

Credit - to remember key elements of a journal entry.

Flash Cards

Glossary

- Journal

The primary book of entry in accounting, recording transactions chronologically.

- Journal Entry

The individual record of a transaction made in a journal.

- Particulars

Accounts involved in a transaction along with a narration.

- Debit

An entry recording the addition of assets or expenses.

- Credit

An entry recording the addition of income or liabilities.

- Ledger Folio (L.F.)

The page number in the ledger where the account can be found.

Reference links

Supplementary resources to enhance your learning experience.