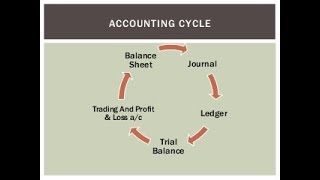

Relationship Between Journal, Ledger, and Trial Balance

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Importance of the Journal

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

The Journal is the first step in our accounting process. It records all transactions as they occur, maintaining a chronological order. Can anyone tell me what that means?

It means we list transactions in the order they happen!

Exactly! This ensures that we do not miss any important financial events. Each Journal entry includes details such as the date, accounts affected, and amounts. Remember, we call these entries 'journal entries.'

So if I buy supplies today and sell a product tomorrow, both will be recorded in the Journal, right?

Absolutely! Each transaction must be recorded as it happens. This is the foundation upon which we build our accounting process.

Function of the Ledger

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Moving on to the Ledger, who remembers how it processes information from the Journal?

The Ledger classifies transactions, right?

Correct! It organizes transactions from the Journal into accounts like Cash, Sales, and Expenses. This makes tracking finances much simpler. What structure does each Ledger account follow?

It's formatted like a T, with debits on one side and credits on the other!

Exactly! This T-account format allows us to see the total debits and credits for each account clearly.

Purpose of the Trial Balance

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Finally, let’s talk about the Trial Balance. Why do we need it?

To check if our totals are correct!

Absolutely! The Trial Balance lists all the account balances from the Ledger, ensuring that the total debits match total credits, thereby confirming our records' accuracy. Can someone explain what this means for the final accounts?

If everything matches, it means we can trust our financial statements!

Exactly. It provides us assurance that our accounting records are reliable, crucial for decision-making.

Interconnection of All Three Components

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let’s discuss how these three parts relate to each other in our accounting system. Can anyone summarize this relationship?

The Journal records first, then those transactions go to the Ledger, and finally, we check everything with the Trial Balance.

Correct! This flow—from Journal to Ledger to Trial Balance—ensures that we maintain accuracy and effective financial reporting. Who can think of a practical example of how these work together?

If I sell a product, that sale goes in the Journal first, then updates the Sales Ledger account, and lastly shows up in the Trial Balance.

Well done! Understanding this flow is essential for grasping how financial data transitions into actionable insights.

Significance in Computerized Accounting

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

In today’s digital age, we use software like Tally and QuickBooks. How do you think these tools differ from manual record-keeping?

They automate the processes we learned about!

Exactly! Journals are filled out via forms, ledgers update automatically, and trial balances can be generated instantly. Why do you think this is advantageous?

It reduces human errors and speeds up reporting!

Perfect! Understanding this application helps us see how foundational concepts adapt in modern contexts.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

The Journal, Ledger, and Trial Balance form the essential components of the accounting cycle. The Journal records transactions sequentially, the Ledger organizes these transactions into accounts, and the Trial Balance checks for accuracy, ensuring that the financial records are correct and complete.

Detailed

Relationship Between Journal, Ledger, and Trial Balance

Understanding the relationship between the Journal, Ledger, and Trial Balance is essential for grasping fundamental accounting practices.

Core Functions

- Journal: The Journal serves as the first point of entry for all financial transactions, recorded chronologically. Each entry reflects a financial occurrence in the business.

- Ledger: The Ledger categorizes these transactions into appropriate accounts, offering a structured format to manage balances for Cash, Sales, Purchases, etc.

- Trial Balance: Finally, the Trial Balance aggregates the ending balances from all Ledger accounts and confirms that total debits equal total credits, acting as a final verification of the accuracy of the accounting data.

Summary

- The Journal initiates the recording process, the Ledger organizes these records, and the Trial Balance ensures everything is correct. Understanding their relationship solidifies accounting concepts, showcasing how raw transactional data transitions into meaningful financial information used for decision-making.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Sequential Process in Accounting

Chapter 1 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Trial

Journal → Ledger → Balance

First record → Classification → Final check

Detailed Explanation

This chunk outlines the sequential nature of accounting processes. First, the Journal is where all transactions are initially recorded. Each entry captures the specifics of a transaction as it happens. Then, these recorded transactions are categorized and summarized in the Ledger, where they are grouped by similar types of transactions under specific accounts. Finally, the Trial Balance stage checks to ensure that the total debits match the total credits, serving as a final verification of completeness and accuracy in accounting.

Examples & Analogies

Think of this process like preparing a report for school. First, you gather all your notes and ideas (Journal phase), then you organize those notes into sections or chapters for easy reference (Ledger phase), and finally, you review your report as a whole to make sure everything is included and looks correct before submitting it (Trial Balance phase).

Roles of Journal, Ledger, and Trial Balance

Chapter 2 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

• Journal records what happened

• Ledger groups similar transactions

• Trial Balance checks accuracy

Detailed Explanation

Each component has a specific role in the accounting process. The Journal's role is to capture every transaction as it occurs, ensuring that all details are accurately recorded in chronological order. The Ledger's role is to categorize these transactions, meaning it sorts them into the appropriate accounts, facilitating the tracking of financial changes over time. Finally, the Trial Balance plays a critical role in verifying the accuracy of these records by ensuring that the total debits equal the total credits, which is essential for maintaining correct financial records.

Examples & Analogies

Using another school analogy, it’s similar to keeping a diary (Journal) where you jot down all your daily activities. Later, you may summarize your days into themes, such as 'Study Days' and 'Family Days' (Ledger). Finally, you might review your diary entries to check if you have correctly covered everything in your school year summary (Trial Balance), ensuring you didn’t miss any details or make any mistakes.

Key Concepts

-

The Journal serves as the original entry point for accounting transactions.

-

The Ledger categorizes and summarizes records from the Journal into accounts.

-

The Trial Balance verifies the accuracy of ledger balances by ensuring debits equal credits.

Examples & Applications

When a company sells a product for cash, the transaction is recorded in the Journal as a cash sale, then posted to both the Cash account and Sales account in the Ledger and finally included in the Trial Balance.

An opening entry for a new accounting period shows cash balance and any initial sales, illustrating how these entries transition from the Journal into the Ledger and then to the Trial Balance.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

In the Journal, the tale begins, recording entries with wins and sins. The Ledger organizes, keeping tabs so balances equal, no room for jabs.

Stories

Imagine a shopkeeper naming Jack who writes every sale in a book on his rack. He then sorts it to accounts, keeping track, and checks it all nice with a balance on his back!

Memory Tools

Remember 'JLT' for Journal, Ledger, Trial - the sequence to keep your accounts reconciled.

Acronyms

JLT

Journal (record)

Ledger (classify)

Trial Balance (check accuracy).

Flash Cards

Glossary

- Journal

The primary book of entry in accounting that records business transactions chronologically.

- Ledger

The principal book of accounts that categorizes transactions from the Journal into various accounts.

- Trial Balance

A statement that shows the balances of all ledger accounts, ensuring that total debits equal total credits.

- Journal Entry

The individual record of a transaction in the Journal.

- DoubleEntry System

An accounting system where every transaction influences at least two accounts, ensuring total debits equal total credits.

Reference links

Supplementary resources to enhance your learning experience.