Format of Trial Balance

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Introduction to Trial Balance Format

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we will explore the format of the Trial Balance. This document is essential for ensuring the accuracy of our accounting records. Can anyone tell me what a Trial Balance summarizes?

It shows the balances of all ledger accounts!

Exactly! It helps us verify that the total debits equal the total credits. Let's look closer at the format. What would you expect to find in a typical Trial Balance list?

I think we would have account names, and their respective debit and credit amounts.

Correct! The format includes three columns: the account name, debit amount, and credit amount. To remember this, think of the acronym 'ADC': Account, Debit, Credit.

So each account essentially has two sides?

Right! Each account will show either a debit or credit amount, and in a balanced Trial Balance, these should equal each other. Let's summarize: the Trial Balance ensures our accounts are balanced and accurate.

Understanding Trial Balance Structure

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

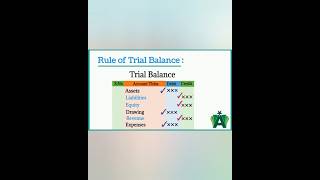

Now, let's discuss how to structure a Trial Balance. When you list accounts, do those accounts belong to any specific category?

They should correspond to the types of accounts: assets, liabilities, revenue, and expenses, right?

Yes! This organization helps in the analysis of financial performance. For example, can anyone explain the overall structure of the Trial Balance?

It starts with listing down accounts, recording their respective debits on one side and credits on the other.

Exactly! After all accounts are listed, we total the debit and credit columns to check the balance. Remember that a balanced Trial Balance indicates no mathematical mistakes in transaction recording.

Can you show us a quick example of how that looks?

Certainly! Let’s create a simple Trial Balance. Imagine we have Cash A/c showing ₹5,000 and Sales A/c with ₹5,000. Would it look balanced?

Yes! The total debits would equal the total credits, which is ₹5,000!

Well summarized! Always remember the structure: accounts, amounts, and balance.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

In the format of a Trial Balance, accounts are systematically listed with their debit and credit balances to ensure that total debits equal total credits. This format is used to check the accuracy of ledger postings and provide a foundation for preparing financial statements.

Detailed

Format of Trial Balance

A Trial Balance is a structured statement that summarizes the balances of all ledger accounts at a specific point in time. The format typically includes:

| Account Name | Debit (₹) | Credit (₹) |

|---|---|---|

| Cash A/c | 5,000 | |

| Sales A/c | 5,000 | |

| Total | 5,000 | 5,000 |

This format illustrates that for every debit recorded in an account, there is a corresponding credit, thereby confirming the arithmetic accuracy of the accounting records. By maintaining the balance, accountants can verify that the double-entry bookkeeping system is functioning correctly and can assist in identifying discrepancies during financial reconciliation.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Structure of the Trial Balance

Chapter 1 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Account Name Debit (₹) Credit (₹)

Cash A/c 5,000

Sales A/c 5,000

Account Name Debit (₹) Credit (₹)

Total 5,000 5,000

Detailed Explanation

The Trial Balance is structured in a table format that consists of two main columns: one for debits and another for credits. Each account that has a balance is listed along with its corresponding amount in either the Debit or Credit column. The total of the Debit column should equal the total of the Credit column, which serves as a verification of the accounting records' accuracy.

Examples & Analogies

Imagine you are keeping a checkbook for your personal finances. At the end of the month, you want to ensure that what you've spent matches what you have on record. You write down all your income on one side (credits) and all your expenses on the other side (debits). If both sides balance, it confirms that you've accounted for your money correctly, similar to how a Trial Balance checks the accounts.

Importance of the Total

Chapter 2 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Total 5,000 5,000

Detailed Explanation

The totals at the bottom of the Trial Balance indicate the sum of all amounts in both the Debit and Credit columns. This is crucial because accounting principles dictate that the total debits must equal total credits, reflecting the fundamental principle of double-entry accounting. If they do not match, it signals that there is an error somewhere in the accounting records that needs to be investigated.

Examples & Analogies

Consider a balancing scale in a grocery store. If the weight on both sides isn't equal, it indicates something isn't right—maybe an item was not accounted for or perhaps there was a mistake in pricing. The same goes for the Trial Balance; the two sides must balance for the accounts to be accurate.

Key Concepts

-

Format: The standard layout of the Trial Balance includes account names and their debit/credit amounts.

-

Purpose: To verify that total debits and total credits are equal, ensuring accuracy.

-

Components: The Trial Balance comprises three columns: Account Name, Debit Amount, and Credit Amount.

Examples & Applications

A simple Trial Balance format may include Cash A/c with ₹5,000 on the debit side and Sales A/c with ₹5,000 on the credit side, totaling ₹5,000 for both.

In a very basic Trial Balance, if Cash A/c is ₹10,000 and Accounts Payable A/c is ₹10,000, it balances perfectly.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

In every Trial Balance, we check our accounts, Debits and credits must match, that’s what counts!

Stories

Imagine a busy marketplace where for every sale made, a record is kept of what was earned and spent. The Trial Balance is like the cashier counting the money to ensure that profit and loss match perfectly!

Memory Tools

Remember 'PAID' for Trial Balance essentials: P - Purpose, A - Accounts, I - Income, D - Debits and Credits.

Acronyms

Use 'ADC' to remember

A-account

D-debit

C-credit.

Flash Cards

Glossary

- Trial Balance

A statement showing the balances of all ledger accounts as on a particular date, ensuring that the sum of debits equals the sum of credits.

- Debit

An entry on the left side of an account representing the increase of assets or expenses.

- Credit

An entry on the right side of an account representing the increase of liabilities, revenue, or equity.

- Ledger Account

An account in the ledger that records all transactions for a specific financial category.

Reference links

Supplementary resources to enhance your learning experience.