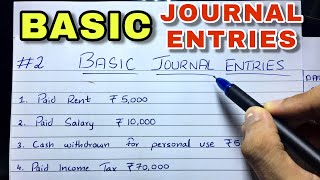

Journal Entries

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Introduction to Journal Entries for Depreciation

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we're going to talk about journal entries related to depreciation. Why is it important for businesses to record depreciation?

I guess to keep track of how much value the assets lose over time?

Exactly! By recording depreciation, companies ensure their financial statements reflect the true value of their assets. Now, can anyone tell me the two main ways we can make journal entries for depreciation?

One is charging depreciation directly to the asset, right?

And the other is through a provision for depreciation!

Good job! Let’s explore these methods in detail.

Charging Depreciation Directly

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Charging depreciation directly involves debiting the Depreciation Account and crediting the Asset Account. What does this mean for the financial statements?

It reduces the value of the asset directly and reflects the expense in the profit and loss statement?

That's correct! This keeps the asset's value at a realistic level while also recording the expense. Can someone tell me when we would use this method instead of the provision method?

I think we’d use it when the depreciation amount isn’t too large or complicated?

Exactly! Simpler assets may not require a provision. Let's now see the second method.

Charging Depreciation through Provision

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

The provision for depreciation method involves debiting the Depreciation Account and crediting a Provision for Depreciation Account. Why do we do this?

So we can set aside money for when we replace the asset eventually?

Yes! It helps companies prepare for the future. What happens at the end of the year?

We need to adjust our accounts, right?

Correct! We debit the Profit & Loss Account and credit the Depreciation Account. This way, all financial effects are recorded properly.

End-of-Year Adjustments

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let’s summarize the end-of-year process. Why do we make these adjustments?

To show how depreciation impacted our net profit for the year.

Exactly! And it gives a realistic view of our asset values. What’s the key takeaway from learning about these journal entries?

It’s important to accurately reflect both asset value and expenses in our reports!

Great! That’s a key part of good financial management.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

The section focuses on the journal entries for accounting depreciation, including direct charging of depreciation to an asset as well as its recording through provision. It also details the end-of-year adjustments to reflect these entries accurately in financial statements.

Detailed

Journal Entries in Depreciation Accounting

In accounting for depreciation, appropriate journal entries are crucial for accurately reflecting the financial status and performance of a business. There are generally two key methods to record depreciation in the journal:

- When Depreciation is Charged Directly: This involves debiting the Depreciation Account and crediting the respective Asset Account. This entry implies that the expense (depreciation) is directly attached to the asset being used.

- When Depreciation is Charged through Provision: This method involves debiting the Depreciation Account and crediting a Provision for Depreciation Account, setting up a separate reserve to account for depreciation.

Finally, at the end of the financial year, businesses need to carry out an adjustment, typically debiting the Profit & Loss Account and crediting the Depreciation Account, reflecting the impact of depreciation on the overall profitability of the company.

This systematic approach ensures transparency and compliance in financial reporting, making it essential knowledge for BTech CSE students studying Management.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Direct Charge of Depreciation

Chapter 1 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

- When Depreciation is Charged Directly:

Depreciation A/c Dr.

To Asset A/c

Detailed Explanation

This journal entry is used when depreciation is charged directly to the asset account. It records the reduction in the asset’s value by debiting the Depreciation Account, which reflects the expense incurred from the asset’s depreciation. The credit to the Asset Account indicates that the actual value of the fixed asset on the balance sheet has decreased.

Examples & Analogies

Imagine you own a car that you purchased for $20,000. Every year, the car loses value due to wear and tear. If you were to record the depreciation directly, you might debit (increase) your Depreciation Account by $2,000 each year that reflects the annual decrease in your car's value. Simultaneously, you'd credit (decrease) your Car Asset Account by the same amount to show that the car is now worth less.

Charging Depreciation through Provision

Chapter 2 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

- When Depreciation is Charged through Provision:

Depreciation A/c Dr.

To Provision for Depreciation A/c

At the end of the year:

Profit & Loss A/c Dr.

To Depreciation A/c

Detailed Explanation

With this journal entry, depreciation is initially recognized in the Depreciation Account, but rather than reducing the asset’s account directly, it is credited to a Provision for Depreciation Account. This approach separates the accumulated depreciation from the asset's value, making it easier to see how much depreciation has been allocated over time. At the end of the year, this entry moves the depreciation expense to the Profit & Loss Account, effectively recognizing the expense for the fiscal year.

Examples & Analogies

Consider a company that owns several machines, and they estimate that these machines will lose value over time. Instead of reducing the machines' asset accounts yearly, the company creates a 'Provision for Depreciation' account. Each year, they debit their Depreciation Account and credit the Provision for Depreciation, tracking it separately. At year-end, they show the expense in their Profit & Loss Account, demonstrating the financial impact of the machinery's depreciation on their profits—perhaps like setting aside money for future repairs rather than directly deducting from the machine's value.

Key Concepts

-

Direct Charging of Depreciation: Involves debit to Depreciation Account and credit to Asset Account.

-

Provision for Depreciation: An account set up to systematically allocate depreciation, preparing for replacements.

-

End-of-Year Adjustment: Reflecting total depreciation in Profit & Loss Account to show impact on financial statements.

Examples & Applications

Example 1: If a company has machinery worth $50,000 with a 10% depreciation rate, the journal entry would debit the Depreciation Account by $5,000 and credit the Asset Account by the same amount.

Example 2: If a company has allocated $2,000 in its Provision for Depreciation Account at the end of the year, it would debit Profit & Loss for $2,000 and credit the Depreciation Account accordingly.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

Assets lose their shine over time, record it right, and all's fine.

Stories

Imagine a wise merchant who writes down the value of each silver coin he trades. He knows that over the years, those coins lose some value as newer coins come into the market.

Memory Tools

DARP - (D)epreciation (A)ccount, (R)eduction of (P)rofit.

Acronyms

PRO - (P)rovision, (R)ecord, (O)ptimize value of assets.

Flash Cards

Glossary

- Depreciation Account

An account used to record the depreciation expenses associated with fixed assets.

- Asset Account

An account that reflects the value of a company's asset at a specific point in time.

- Provision for Depreciation

A reserve created to account for depreciation of assets, preparing for future asset replacement.

- Profit & Loss Account

A financial statement that summarizes revenues, costs, and expenses to show net profit or loss over a period.

Reference links

Supplementary resources to enhance your learning experience.