Provisions vs Reserves

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Understanding Provisions

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, let's discuss provisions. Provisions are mandatory amounts that companies must set aside to meet specific liabilities or expected expenses. Can anyone tell me why this is important?

I think it's to be prepared for future costs, especially if they’re uncertain.

Exactly! Provisions ensure that a company doesn’t show inflated profits by ignoring liabilities. Remember, they reduce net profit because they are treated as expenses.

So, they directly affect the financial statements?

Yes, they show a more accurate financial position. Let's also remember the mnemonic: 'Provisions Protect Profits'.

Got it! But what happens if a company doesn't make these provisions?

Great question! Without provisions, the company might mislead stakeholders about its profitability and financial health.

In summary, provisions are compulsory, adjust profits downwards, and project an accurate future liability.

Understanding Reserves

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now let’s shift gears and talk about reserves. Who can define what reserves are?

Reserves are funds set aside from profits to strengthen a company financially.

Correct! They don't reduce net profit like provisions do because they are an appropriation of profit. Can anyone think of why companies might want to create reserves?

To have funds available for unforeseen circumstances?

Exactly! Reserves act as a financial cushion. Think of the acronym 'R.E.S.T.' which stands for Reserve for Emergencies and Strategic Transfers.

And they’re not legally required, right?

That's right! Reserves are not mandatory, making them a strategic decision by the management. In summary, reserves are used to improve financial health and are not treated as expenses, thus preserving profit levels.

Comparative Analysis

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Alright, let’s create a summary comparison between provisions and reserves. Who can list at least two differences?

Provisions are compulsory and reduce net profit, while reserves are not always mandatory and don't affect profit directly.

Exactly! Can anyone highlight the impact of both on financial statements?

Provisions show as an expense on the income statement, while reserves are shown as part of retained earnings.

Good! This distinction is key for understanding financial health disclosures. Keep in mind that understanding these differences helps in financial analysis!

To sum up, provisions are about preparation for liabilities while reserves focus on financial robustness.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

Provisions are mandatory allocations made to meet specific liabilities, directly impacting profit while reducing net income. In contrast, reserves are often discretionary financial appropriations that aim to strengthen a company's financial position without affecting profit directly.

Detailed

Provisions vs Reserves

In accounting, the distinction between provisions and reserves is crucial for understanding how each affects financial statements and the overall financial position of a business.

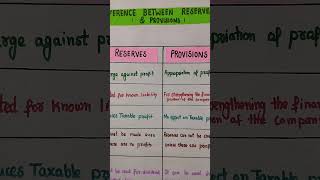

- Purpose: Provisions are created to account for specific liabilities that a company anticipates, ensuring adequate coverage for future expenses (e.g., depreciation). Reserves, on the other hand, are funds set aside from profits to enhance the financial stability of the company, offering a cushion against unexpected future needs.

- Compulsory Nature: Provisions are compulsory under accounting rules in the case of certain liabilities, such as depreciation, because they reflect a genuine anticipation of future financial outflow. Reserves don't possess a similar legal obligation and are more about prudent financial management.

- Accounting Treatment: Provisions are recorded as an expense on the income statement, which directly reduces the net profit of the company. Reserves, conversely, are an appropriation of profit and do not affect the company’s profit directly since they are taken from retained earnings.

- Effect on Profit: The establishment of provisions decreases the net profit of a company because they are treated as expenses. In contrast, transfers to reserves do not impact the profit directly; they merely represent an allocation of available profits into a retained earnings reserve.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Definition of Provision and Reserve

Chapter 1 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

| Basis | Provision | Reserve |

|---|---|---|

| Purpose | Made to meet a specific liability | Made to strengthen financial position |

Detailed Explanation

This chunk defines the primary differences between provisions and reserves in accounting. A provision is created specifically to meet certain liabilities that a company anticipates it will need to pay in the future. For example, a company might set up a provision for bad debts if it expects some of its customers will not pay their invoices. On the other hand, reserves are created more generally to improve the overall financial position of the company, acting as extra funds that can be used for future needs or emergencies.

Examples & Analogies

Think of provisions as a savings account set aside for a specific purpose, like saving for a vacation that you plan to take next year. The reserve would be like an emergency fund that you keep accessible for any unexpected expenses that may arise.

Mandatoriness of Provisions and Reserves

Chapter 2 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

| Basis | Provision | Reserve |

|---|---|---|

| Compulsory | Yes, in case of depreciation | Not always mandatory |

Detailed Explanation

This chunk discusses the legal requirements surrounding provisions and reserves. Provisions are often mandatory, particularly for certain liabilities like depreciation, where accounting standards require businesses to reflect potential losses accurately. Reserves, meanwhile, are not always compulsory; companies can decide whether or not to create reserves based on their financial strategies and needs.

Examples & Analogies

Imagine a student is required to save a certain amount of money for tuition fees (provision), while setting aside extra money for a potential road trip is a personal choice (reserve).

Accounting Treatment of Provisions vs Reserves

Chapter 3 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

| Basis | Provision | Reserve |

|---|---|---|

| Accounting Treatment | Treated as an expense | Appropriation of profit |

Detailed Explanation

In accounting, provisions are treated as an expense, meaning they reduce the net profit reported in financial statements. This is because they account for anticipated costs. Conversely, reserves are considered an appropriation of profit, which means that they do not impact the reported profit figure directly. Instead, reserves represent profits that have been set aside for specific purposes.

Examples & Analogies

Consider a household budget: the money put aside for monthly utility bills is like a provision—it explicitly decreases your disposable income because you know you'll have to spend it. The money you set aside for a future home renovation is like a reserve—it doesn’t reduce your current spending, but it represents a choice to allocate profits for future needs.

Effects on Profit

Chapter 4 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

| Basis | Provision | Reserve |

|---|---|---|

| Affect on Profit | Reduces net profit | Profit remains unaffected |

Detailed Explanation

This chunk explains how provisions and reserves impact reported profit. When a provision is created, it causes a reduction in net profit because it is recorded as an expense. For example, if a company sets aside money for employee bonuses, that amount will decrease its profit for the reporting period. In contrast, reserves do not affect the profit when they are created; they simply reflect retained earnings that could be used in the future.

Examples & Analogies

Think of it as an athlete saving for retirement. If a portion of their earnings is set aside for retirement (provision), it counts against their present income. However, any prize money they decide to save for a potential future tournament (reserve) does not reduce their current earnings—it simply exists in their overall financial picture.

Key Concepts

-

Provision: A mandatory allocation for anticipated liabilities.

-

Reserve: An appropriation of profits to reinforce financial strength.

-

Impact on Profit: Provisions reduce profit; reserves do not.

-

Compulsory Nature: Provisions are legally required; reserves are not.

Examples & Applications

A manufacturing company sets aside a provision for warranty claims to cover potential future costs.

A retail company creates reserves from its profits to fund future expansion activities.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

Provisions for costs we foresee, to guard against future liability.

Stories

Imagine a knight preparing for battle, gathering not only his sword but also food and supplies. Just like he prepares for uncertainties, companies create provisions to safeguard against potential expenses.

Memory Tools

Remember 'PPA' for Provisions Protect Assets, while RRE stands for Reserves Reinforce Earnings.

Acronyms

Use 'PARE' - Provisions Account for Required Expenses and 'SAFE' - Savings Appropriated for Future Earnings to remember the concepts.

Flash Cards

Glossary

- Provision

A mandatory account set aside for specific future liabilities.

- Reserve

An appropriation of profits set aside to bolster financial strength.

Reference links

Supplementary resources to enhance your learning experience.