Objectives of Accounting

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Recording Transactions

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we're going to discuss the first objective of accounting: recording transactions. Why do you think it’s important to record every transaction systematically?

I think it's important because it helps keep things accurate.

That's right! Accurate recording ensures that nothing is overlooked. How do you think this might impact financial statements?

If transactions aren’t recorded correctly, the financial statements will be wrong.

Exactly! Remember the acronym 'ARE'—Accuracy, Relevance, and Efficiency—when discussing financial recording.

So, if we miss a transaction, we might not know how profitable our business actually is?

Yes! And that’s why recording is crucial.

Let’s summarize: The key point is that systematic and accurate recording of financial transactions is fundamental for ensuring reliable financial reporting.

Classifying and Summarizing Financial Data

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Next, let’s talk about classifying and summarizing financial data. Why do you think categorizing transactions is essential?

It helps to see where the money is going and what kinds of transactions we have.

Good insight! By categorizing transactions into assets, liabilities, income, and expenses, we can maintain an overview of financial health. Can anyone give me an example of how different categories might look?

Like separating cash from inventory for assets?

Exactly! That helps in understanding the business as a whole. We can use the mnemonic 'A-L-I-E'—Assets, Liabilities, Income, and Expenses—to remember these categories.

That’s helpful! So, summarizing them helps in creating financial statements?

Precisely! Now let's wrap up this session: Classifying and summarizing provides clarity on financial statements and helps in performance assessment.

Providing Information for Decision Making

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now, we will discuss the third objective: providing financial information for decision making. Why do you think stakeholders need this information?

So they can make the best choices for the company—like investing or cutting costs.

Right! This information is crucial for decisions about investments, funding, and strategy. What reporting tools do you think accounting uses to provide this information?

Financial statements, like the income statement and balance sheet.

Absolutely! Utilizing 'BCE'—Balance sheet, Cash flow statement, and Income statement—can help us remember the primary tools. How do you think this information influences business success?

It shows where to invest or save money or if any changes are necessary!

Great point! In summary, financial information derived from accounting is pivotal for making informed decisions regarding business operations.

Ensuring Legal Compliance

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's now focus on the fourth objective, which is ensuring legal compliance. Why should businesses comply with accounting laws and standards?

To avoid fines and keep their reputation clean.

Exactly! Compliance is critical not only for avoiding legal issues but also for building trust with stakeholders. How can non-compliance impact a company?

It could lead to legal penalties or maybe even bankruptcy!

Yes! A useful mnemonic here is 'CLIP'—Compliance, Laws, Integrity, Protecting assets. So what do we take away from this session?

That following laws helps protect the company and its stakeholders!

Correct! In summary, ensuring legal compliance safeguards the business and upholds its reputation in the marketplace.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

Accounting serves four main objectives: the systematic recording of transactions for accuracy, classifying financial data into meaningful categories for analysis, supplying crucial financial information for decision-making, and ensuring adherence to legal standards and regulations. These objectives help stakeholders understand the financial health of the organization.

Detailed

Objectives of Accounting

Accounting plays a vital role in managing finances within an organization, and its main objectives include:

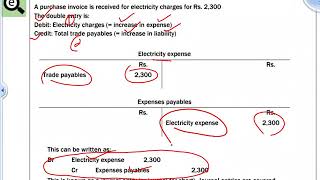

- Recording Transactions: Accounting is primarily about systematically recording all financial transactions, which is crucial for maintaining accuracy and completeness in reporting.

- Classifying and Summarizing Financial Data: This involves organizing financial transactions into appropriate categories (assets, liabilities, income, expenses) which assists in providing a clear snapshot of a business’s financial health.

- Providing Financial Information for Decision Making: The information compiled and processed through accounting enables business owners, managers, and other stakeholders to make informed decisions based on financial reports and statements.

- Ensuring Legal Compliance: Accounting ensures adherence to tax laws and financial reporting standards set forth by governing bodies, which is essential for legal compliance and avoiding penalties.

Understanding these objectives is important as they lay the foundation for effective financial management and informed decision-making.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Recording Transactions

Chapter 1 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

● Recording Transactions

○ The primary objective of accounting is to systematically record all financial transactions that occur within a business, ensuring accuracy and completeness.

Detailed Explanation

The first objective of accounting is to keep a detailed and systematic record of every financial transaction that takes place in a business. This means that every sale, purchase, expense, and income must be logged accurately and completely. This systematic approach helps ensure that no important financial data is overlooked, which is crucial for understanding the business’s performance over time.

Examples & Analogies

Imagine you are keeping a diary of your daily expenses. Each time you buy something, you write it down immediately. This practice helps you track where your money goes and prevents you from forgetting smaller purchases. In accounting, this process is similar, where every transaction is logged in the books to give a complete picture of the business's financial activities.

Classifying and Summarizing Financial Data

Chapter 2 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

● Classifying and Summarizing Financial Data

○ Accounting organizes and classifies financial transactions into categories, such as assets, liabilities, income, and expenses, to present an overview of the financial health of a business.

Detailed Explanation

Once financial transactions are recorded, the next step in accounting is to classify and summarize this information. This involves grouping transactions into different categories, such as assets (what the business owns), liabilities (what it owes), income (money coming in), and expenses (money going out). By organizing financial data in this way, it becomes easier to understand the overall financial health of the business through comprehensive reports.

Examples & Analogies

Think of sorting your personal expenses into categories like groceries, rent, and entertainment. By categorizing your spending, you can see where most of your money goes and make informed decisions about budgeting. Similarly, businesses classify their financial activities to easily assess their performance and make strategic decisions.

Providing Financial Information for Decision Making

Chapter 3 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

● Providing Financial Information for Decision Making

○ Accounting helps business owners, managers, and stakeholders make informed decisions based on financial reports and statements.

Detailed Explanation

One of the key objectives of accounting is to provide critical financial information that assists in making sound business decisions. Financial reports, which are based on the collected and classified data, are used by owners, managers, and other stakeholders to evaluate the company's performance, assess risks, and determine future strategies. This enables informed decision-making regarding investments, cost management, and other operational aspects.

Examples & Analogies

Consider a restaurant owner reviewing monthly financial reports to decide whether to expand the menu or cut certain items that aren’t selling well. These financial statements provide insights into sales, costs, and profits, guiding the owner's decisions. Just like in the restaurant example, businesses use accounting reports to navigate their strategic paths.

Ensuring Legal Compliance

Chapter 4 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

● Ensuring Legal Compliance

○ Accounting ensures that businesses comply with tax laws, financial reporting standards, and regulations set by governing bodies like the Income Tax Department and the Securities and Exchange Board of India (SEBI).

Detailed Explanation

Another important objective of accounting is to ensure that businesses adhere to legal obligations regarding financial reporting and taxation. This involves following the required standards and regulations set by government bodies, such as filing tax returns and preparing financial statements according to established guidelines. Compliance not only helps avoid legal penalties but also builds trust with stakeholders and the public.

Examples & Analogies

Think of it like following traffic rules while driving. If you abide by the laws, you reduce the risk of getting a ticket or causing an accident. Businesses need to follow accounting regulations to avoid penalties and maintain a good reputation. Just as responsible driving ensures safety, maintaining accounting compliance protects a business from legal issues.

Key Concepts

-

Recording Transactions: The importance of accurate financial documentation.

-

Classifying Financial Data: Organizing financial transactions into clear categories.

-

Financial Information: Providing insights for decision-making.

-

Legal Compliance: Ensuring adherence to laws for business integrity.

Examples & Applications

Using a sales receipt to record a transaction in a company's accounting system.

Categorizing business expenses into operating costs, marketing expenses, and administrative expenses.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

In accounting, every note, every entry, keeps the company afloat.

Stories

Imagine a captain steering a ship; without accurate logs of wind and tide, the voyage would be a fluke. Just like a business needs accurate records to navigate success.

Memory Tools

Remember 'CLIP' for Compliance, Laws, Integrity, Protecting assets in accounting.

Acronyms

A-L-I-E for Assets, Liabilities, Income, and Expenses, the backbone categories in accounting.

Flash Cards

Glossary

- Recording Transactions

The systematic process of documenting all financial transactions in an organization for accuracy and completeness.

- Classifying Financial Data

The organization of financial transactions into categories such as assets, liabilities, income, and expenses.

- Financial Information

Data derived from accounting that aids stakeholders in making decisions.

- Legal Compliance

The process of ensuring adherence to laws and regulations related to financial reporting.

Reference links

Supplementary resources to enhance your learning experience.