Conservatism (Prudence)

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Understanding Conservatism in Accounting

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we'll explore the conservatism principle in accounting, also known as prudence. This principle suggests that we should anticipate no profits but provide for all possible losses. Can someone explain why this might be essential for financial reporting?

I think it helps to ensure that companies don't overstate their financial health, right?

Exactly, Student_1! By doing this, companies avoid misleading stakeholders about their profitability. It's about protecting the interests of investors. What do you think might happen if a company didn't follow this principle?

They might look more profitable than they actually are, which could lead to financial crises down the line.

Great point, Student_2! Now, let's remember the mnemonic 'ALWAYS SAFE' - Always recognize losses, but be Safe with profits. This helps us recall the essence of conservatism.

So we should recognize a provision for doubtful debts even if they haven't defaulted yet?

Yes, that's the right example! Recognizing such provisions is a practical application of conservatism.

In summary, conservatism ensures reliability and prevents financial misrepresentation. Always be aware of potential losses!

Application of Conservatism Principle

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's dive into how conservatism is applied in real situations. Can anyone give me an example of how conservatism might impact financial decisions?

I think if a business expects a decline in sales, they should reduce their revenue expectations.

Absolutely right, Student_4! This aligns with conservatism, where they account for possible drops in income rather than inflating potential revenue. What about reporting liabilities?

They should report them as soon as they are possible, even if it's uncertain if they'll materialize into actual losses.

Well put! This prudent approach helps maintain transparency and ensures investors are informed about the risks involved. Would someone like to add another example?

Like when a company creates a rainy day fund for potential unexpected costs?

Yes, that's an excellent example! To conclude, by implementing conservatism, businesses create a safety net protecting their financial integrity.

Revisiting Key Concepts of Conservatism

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Alright, let's review what we've covered about conservatism. Why is the principle considered essential in accounting?

It helps avoid the overestimate of profits and the understatement of losses.

Exactly! $ALWAYS SAFE$ is a helpful way to remember it. What are some challenges concerning this principle?

It can lead to overly cautious financial statements that might mislead investors about company potential.

That's an insightful observation, Student_2! While it's important to be cautious, over-cautiousness can lead to missed opportunities. Let's ensure that we balance prudence with a realistic outlook.

In summary, the conservatism principle is key to honest reporting. Remember, we're always better safe than sorry!

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

The conservatism principle is a critical accounting convention that advises accounting for expenses and liabilities as soon as possible while recognizing revenues only when they are certain and earned. This approach protects stakeholders by ensuring financial statements do not overstate a company’s financial health.

Detailed

Detailed Summary

The conservatism principle, also referred to as prudence, is a fundamental accounting convention that directs accounting professionals to err on the side of caution when reporting financial data. The principle states that potential losses should be anticipated, and thus, expenses and liabilities should be recognized promptly. Conversely, revenues should only be acknowledged when they are certainly realized or receivable. This practice aims to provide a more realistic view of a company's financial status and ensures that stakeholders, such as investors and creditors, receive reliable financial information.

For instance, businesses often create provisions for doubtful accounts to prepare for potential losses from unpaid debts, even if those debts are still considered collectible. By adhering to the conservatism principle, financial statements maintain integrity and bolster stakeholder trust, as they present a realistic outlook on profitability and financial stability.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Definition of Conservatism

Chapter 1 of 3

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

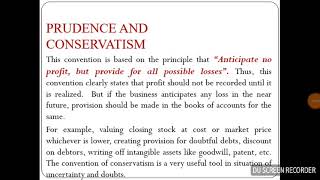

Anticipate no profit but provide for all possible losses. Recognize expenses and liabilities as soon as possible, but revenues only when they are certain.

Detailed Explanation

The principle of conservatism, also known as prudence, encourages accountants to be cautious when making predictions about profits. This means that they should only recognize revenue when it is certain and be proactive in acknowledging possible expenses or losses. The goal is to avoid overstating the financial health of a business. This approach helps provide a more conservative and cautious view of the company's financial position, thereby safeguarding stakeholders against unrealistic expectations.

Examples & Analogies

Imagine a farmer predicting the harvest of his crops. Instead of assuming maximum potential yield and planning his expenses based on that, he only plans based on previous harvests to ensure his expectations are realistic. If he thinks a drought might cause loss, he prepares for that scenario. This cautious approach mirrors the conservatism principle, ensuring that the farmer doesn't face financial difficulties if his predictions don't pan out.

Recognizing Expenses and Liabilities

Chapter 2 of 3

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Recognize expenses and liabilities as soon as possible, but revenues only when they are certain.

Detailed Explanation

Under the conservatism principle, companies are expected to acknowledge and record expenses and liabilities quickly. This means that if a business anticipates an expense, such as potential debts that may not be recovered, it should record that expense immediately even if the actual loss hasn't occurred yet. In contrast, profits or revenues should only be recorded when they are confirmed and not just expected, protecting the business from appearing more prosperous than it truly is.

Examples & Analogies

Think of a restaurant that has given away free meals to promote itself, expecting that customers will return to pay later. Under the conservatism principle, the restaurant should not count those free meals as profits until actual payments are received from customers. Just as a person wouldn’t spend money they haven’t yet received, the restaurant must record revenue only when it is assured.

Provision for Doubtful Debts

Chapter 3 of 3

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Example: Creating provision for doubtful debts even if the debt hasn’t defaulted yet.

Detailed Explanation

A common application of the conservatism principle in accounting is the creation of provisions for doubtful debts. This means that an organization anticipates that some of its customers may not pay their outstanding invoices. Therefore, even before a debt is confirmed to be unpaid, the company will recognize a provision on its financial statements to reflect that risk. This not only reduces the reported profit but also gives a clearer picture of potential future losses.

Examples & Analogies

Consider a credit card company that lends money. Knowing that some borrowers may not pay back their loans, the company sets aside a portion of its revenue as a provision for these potential losses. It’s similar to having an emergency fund; you set aside money recognizing unforeseen circumstances might arise, ensuring you're prepared should the worst happen.

Key Concepts

-

Conservatism Principle: Advises recognizing losses and liabilities while postponing revenue recognition until certainty is established.

-

Provision for Doubtful Debts: An estimation of potential losses from credit sales deemed uncollectible.

Examples & Applications

Creating a provision for doubtful debts to handle potential customer defaults.

A tech company reflects reduced sales expectations in their financial forecasts to account for market instability.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

When profits seem near, don’t you cheer, anticipate loss, and be clear.

Stories

A farmer who only plants seeds for certain harvests teaches us not to overestimate our returns, reminding us of the importance of preparing for failed crops.

Memory Tools

Remember 'ALWAYS SAFE', Always brace for loss, but be Safe about gains.

Acronyms

C.L.E.A.R - Conservatism Leads to Early Assessment of Risks.

Flash Cards

Glossary

- Conservatism (Prudence)

An accounting principle that advises anticipating no profit but providing for all possible losses; recognizing expenses and liabilities as soon as possible, while revenues are recognized only when they are certain.

- Provision for Doubtful Debts

An accounting entry that recognizes potential future losses due to customers failing to pay their debts.

Reference links

Supplementary resources to enhance your learning experience.