Going Concern Concept

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Introduction to Going Concern Concept

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we'll explore the 'Going Concern Concept.' This concept assumes that a business will continue its operations indefinitely unless stated otherwise. Why do you think this is important for financial statements?

I think it helps investors understand if a business is stable or not.

It probably impacts how assets are valued too!

Exactly! If a business is assumed to continue operating, assets aren't recorded at liquidation values but rather at their historical cost, ensuring a more accurate financial picture.

Implications of Going Concern Concept

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now that we understand what the Going Concern Concept is, let's talk about its implications. What happens if a business is not going concern?

Wouldn't that mean they have to prepare their financials differently?

That's right! If a business is not a going concern, it has to report its assets at their liquidation value, which can show a very different financial picture.

Examples of Going Concern Concept

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's consider a practical example. If a company has significant debt and is facing bankruptcy, how does this affect the going concern assumption?

It might mean they can't continue operating, so they wouldn’t prepare their financials under the going concern assumption anymore.

Absolutely! This shift informs stakeholders of potential risks and impacts decisions.

Concluding Discussion on Going Concern

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

What is the main takeaway regarding the Going Concern Concept?

It's crucial for understanding how to interpret a company's financial health.

And it affects how we value assets on the balance sheet.

Exactly! The Going Concern Concept is fundamental for stakeholders to accurately assess a company's financial situation.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

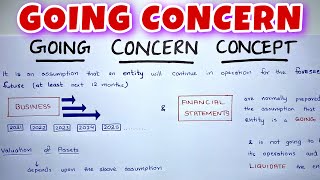

The Going Concern Concept is a fundamental accounting principle that presumes an entity will continue to operate for the foreseeable future. This concept is crucial for determining the valuation of assets and liabilities and plays a significant role in financial reporting.

Detailed

Going Concern Concept

The Going Concern Concept is a vital accounting principle that assumes a business will continue to operate indefinitely unless there is evidence to the contrary. This principle affects how assets are valued and inhibits their recording at liquidation values. For instance, if a company is expected to continue its operations, assets such as buildings and equipment are recorded at their purchase price rather than their potential liquidation value. This approach ensures that financial statements provide a true reflection of the company's operational status and long-term viability, enabling stakeholders to make informed investment and management decisions.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Understanding Going Concern Concept

Chapter 1 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

It is assumed that the business will continue its operations indefinitely unless stated otherwise.

Detailed Explanation

The going concern concept is a fundamental principle in accounting that assumes a business will continue to operate into the foreseeable future. This means that the financial statements of the business are prepared with the expectation that it is not planning to liquidate or cease operations in the near future. As such, this principle influences how assets and liabilities are valued, ensuring they reflect their ongoing usage rather than potential liquidation values.

Examples & Analogies

Imagine a bakery that has been serving customers successfully for years. If the bakery owner decides to take out a loan to expand the business, the bank looks at the bakery's financial health with the assumption that it will continue to make profits and remain in business. They won't evaluate the bakery's value based on how much it could sell its ovens for today, but rather on the future earnings potential of those ovens being used to bake for years to come.

Impact on Asset Valuation

Chapter 2 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

This affects asset valuation and depreciation. Assets are not recorded at liquidation value.

Detailed Explanation

Under the going concern assumption, assets are valued based on their historic costs and their expected future benefits, not their liquidation values. For example, when accounting for depreciation—how much value an asset loses over time—it is calculated based on the asset's expected life and usage in the business, rather than what the asset would be worth if the business sold it off immediately. This helps present a clearer picture of a business's financial position and operational capabilities.

Examples & Analogies

Consider a delivery truck owned by a logistics company. If the business is operating under the premise that it will continue functioning, the truck's value will be calculated based on its cost and how long it will be used for deliveries. However, if the logistics company was going out of business, they would assess the truck's current sale value, which could be significantly lower. The going concern assumption ensures the company considers the truck's utility rather than just its immediate financial return.

Key Concepts

-

Going Concern: A key assumption in accounting that suggests businesses will continue to operate indefinitely.

-

Impact on Asset Valuation: Under this assumption, assets must be valued at historical cost rather than liquidation value.

Examples & Applications

A company presumes it will operate for the next decade, thus its assets are recorded at their purchase prices.

If a company is struggling and unable to continue, it must reassess its asset valuations to reflect potential liquidation amounts.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

If a business isn't nearing the end, its values won't bend, they're assets to defend.

Stories

Imagine a tree that keeps growing and producing fruit. As long as it’s healthy, it can keep going. This is like a going concern, where the business's future looks bright.

Memory Tools

Goes On: G for 'Going,' O for 'Operating,' S for 'Sustainably' - remember that business goes on!

Acronyms

GCC - Going Concern Concept

Helps us remember the three key aspects

Flash Cards

Glossary

- Going Concern Concept

An assumption that a business will continue its operations indefinitely unless stated otherwise.

- Liquidation Value

The estimated amount that an asset would realize upon its sale in a liquidation scenario.

Reference links

Supplementary resources to enhance your learning experience.