Adjustments in Final Accounts

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Outstanding Expenses

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's start with outstanding expenses. Can anyone tell me what they think these are?

Are they expenses that have already happened but haven’t been recorded yet?

Exactly! Outstanding expenses are incurred but not yet entered into the accounts. Why is it important to account for these?

So that we can show the true costs incurred during the accounting period?

That's correct! These expenses are added to the Profit & Loss account and recognized as a liability in the Balance Sheet. A helpful mnemonic is 'O.E.L' for Outstanding Expenses = Liability.

Got it! O.E.L!

Prepaid Expenses

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now, what about prepaid expenses? Who can define them?

Prepaid expenses are payments made in advance for services or goods not yet received?

Exactly! They are deducted from the related expense in the Profit & Loss account. How do we treat them in the Balance Sheet?

We show them as an asset!

Right! You can remember this with the saying 'Prepaid is Paid Before', highlighting they're considered an asset.

Accrued Income

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Next, let's talk about accrued income. Who can share what they think it is?

It’s money earned but not yet received, right?

That's it! It needs to be added to the income in the Profit & Loss account and appears as an asset on the Balance Sheet. To simplify this, think of the acronym 'A.I.'. Can anyone guess what that stands for?

'Accrued Income'?

Correct! Always remember, accrued means earned, but not yet received.

Income Received in Advance

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now, let’s discuss income received in advance. Who can provide a definition?

It’s when we receive payment for a service or product we haven’t delivered yet.

Perfect! This income must be deducted from revenue in the Profit & Loss account and recorded as a liability. Remember the mnemonic 'A.V.' for Advance Income = Liability.

I like that! A.V. - Advance is a Liability!

Depreciation and Bad Debts

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Finally, we need to cover depreciation and bad debts. Can someone explain what depreciation means?

It’s the reduction in value of an asset over time due to wear and tear.

Exactly! It’s charged in the Profit & Loss account and also deducted from assets on the Balance Sheet. How about bad debts?

Those are debts that we won’t be able to collect.

Spot on! They’re charged to the Profit & Loss account and deducted from debtors. To remember these, think of the acronym 'D.B.' for Depreciation and Bad debts both affect the Bottom line!

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

This section explores the various types of adjustments necessary for final accounts, including how they affect the Profit & Loss account and the Balance Sheet. Examples include outstanding expenses, prepaid expenses, accrued income, and more.

Detailed

Adjustments in Final Accounts

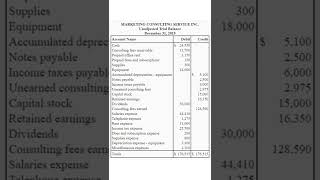

Adjustments are crucial in final accounts to accurately reflect all financial transactions relevant to a given accounting period. As not all items may be recorded within the regular accounting cycle, adjustments cater to items that need to be included to ensure that financial statements portray a true and fair view of the financial performance and position of the business.

The main types of adjustments include:

- Outstanding Expenses: These are expenses that have been incurred but not yet recorded. They are added to the related expense in the Profit & Loss account and recorded as a liability in the Balance Sheet.

- Prepaid Expenses: Expenses that have been paid in advance are deducted from the related expense and shown as an asset in the Balance Sheet.

- Accrued Income: Income that is earned but not yet received is added to the income in the Profit & Loss account and shown as an asset on the Balance Sheet.

- Income Received in Advance: This is income that has been received before it is earned. It is deducted from income in the Profit & Loss account and shown as a liability in the Balance Sheet.

- Depreciation: This adjustment represents the allocation of the cost of an asset over its useful life. It is charged in the Profit & Loss account and deducted from the asset in the Balance Sheet.

- Bad Debts: Debts that are deemed uncollectible are charged to the Profit & Loss account and deducted from debtors in the Balance Sheet.

These adjustments ensure compliance with accounting standards and provide stakeholders with accurate financial reports.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Outstanding Expenses

Chapter 1 of 6

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Add to concerned expense in P&L, show as liability in BS

Detailed Explanation

Outstanding expenses are costs that a business has incurred but has not yet paid by the end of the accounting period. For example, if a company has received services like electricity or internet but has not yet settled the bill, this expense still needs to be recorded. In the Profit & Loss (P&L) account, the outstanding expenses are added to the related expense category, increasing the total expenses. In the Balance Sheet (BS), these amounts are reported as a liability, indicating that the company owes this money.

Examples & Analogies

Think of a person who regularly eats at a restaurant but decides to pay their bill the following month. Even though they enjoyed their meal and benefited from it this month, they still owe the restaurant money for the service in their current period. Similarly, businesses record this 'owed' amount as outstanding expenses.

Prepaid Expenses

Chapter 2 of 6

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Deduct from concerned expense, show as asset in BS

Detailed Explanation

Prepaid expenses refer to payments made for services or goods that will be received in future accounting periods. For instance, if a company pays its insurance premium for six months in advance, it should not record this entire amount as an expense in the current accounting period because part of it pertains to future periods. In the P&L, the prepaid expense is deducted from the total expense, and on the BS, it is shown as an asset since the company has a right to services or goods that it has already paid for.

Examples & Analogies

Consider a subscription service that you pay for a year in advance. Even if you pay for it now, you are actually 'using' that subscription over the next 12 months. Just like the subscription, when businesses pay for something in advance, they record it as a prepaid expense, acknowledging that they still have a benefit coming in the future.

Accrued Income

Chapter 3 of 6

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Add to income in P&L, show as asset in BS

Detailed Explanation

Accrued income represents revenue that has been earned but not yet received by the end of the accounting period. For instance, if a consulting firm completes a project in December but will only bill the client in January, this income must still be recognized in December's financial reports. In the P&L, this accrued income is added to total income since it is revenue that the business has earned during the period. In the BS, it is reported as an asset because the business expects to receive this money soon.

Examples & Analogies

Imagine a freelancer who finishes a project for a client in December, but the payment is not due until January. Although the money isn't in their account yet, they still earned that income in December, similar to how businesses account for accrued income.

Income Received in Advance

Chapter 4 of 6

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Deduct from income in P&L, show as liability in BS

Detailed Explanation

Income received in advance refers to money received by a business before it has actually earned that income. An example would be a magazine publisher that receives payments for magazine subscriptions before the magazines are published. In the P&L, this amount is deducted from total income since it doesn’t reflect actual earned revenue. In the BS, it is shown as a liability because the company still owes the subscribers their magazines in the future.

Examples & Analogies

Think of ordering a pizza. If you pay for the pizza ahead of time, you haven't yet received the product; you're entitled to it in the future. Hence, the restaurant has a liability to fulfill your order, similar to how businesses treat income received in advance.

Depreciation

Chapter 5 of 6

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Charge in P&L, deduct from asset in BS

Detailed Explanation

Depreciation is the process of allocating the cost of tangible assets over their useful lives. For example, if a company buys machinery for ₹100,000 and estimates it will be useful for 10 years, it might record an annual depreciation expense of ₹10,000. This expense is charged in the P&L account, reducing the net profit. In the BS, the machinery's value is deducted by the same amount, reflecting its decreased value over time.

Examples & Analogies

Imagine buying a new car. As time passes, the car loses value due to wear and tear. You wouldn’t expect to sell it for the same price you paid after a few years. Similarly, businesses factor in this loss of value through depreciation, showing the true worth of their assets.

Bad Debts

Chapter 6 of 6

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Charge to P&L, deduct from debtors in BS

Detailed Explanation

Bad debts are amounts owed by customers that are unlikely to be collected. For instance, if a business sells goods on credit and later realizes that a customer has gone bankrupt, the owed amount is deemed uncollectible. The business must charge this amount as an expense in the P&L, reducing overall profit. Additionally, in the BS, it is deducted from the debtors (accounts receivable) since that amount will no longer be received.

Examples & Analogies

Think of lending money to a friend who promises to pay you back, but later you find out they can’t. You’d recognize that you won’t get that money back—just like businesses must account for bad debts, recognizing that they may not receive what is owed.

Key Concepts

-

Outstanding Expenses: Unrecorded expenses that are recognized to ensure accuracy in accounts.

-

Prepaid Expenses: Expenses paid beforehand, recognized as assets.

-

Accrued Income: Income that has been earned but not yet collected.

-

Income Received in Advance: Payments received before the provision of service, treated as liabilities.

-

Depreciation: A systematic reduction of the value of fixed assets over their useful life.

-

Bad Debts: Uncollectible debts that reduce the overall profitability.

Examples & Applications

If a company incurred electricity expenses of ₹10,000 for December but has not recorded it yet, it needs to account for outstanding expenses.

If a business pays ₹5,000 for insurance coverage for the next year in January, this amount must be treated as a prepaid expense.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

For every cost that’s missed, we list; Outstanding expenses we cannot resist!

Stories

Imagine a shopkeeper who pays for insurance six months in advance. When the bill comes, they remember it's a prepaid expense. They count it as an asset, ready to cover future costs.

Memory Tools

M.A.P. - Monitor Accrued Payments to remember to account for accrued income correctly.

Acronyms

D.B. – Depreciation and Bad debts. Both reduce profit and understanding this helps balance accounts.

Flash Cards

Glossary

- Outstanding Expenses

Expenses incurred but not yet recorded in the accounts.

- Prepaid Expenses

Payments made in advance for future expenses.

- Accrued Income

Income earned but not yet received or recorded.

- Income Received in Advance

Payments received before the delivery of goods or services.

- Depreciation

Allocation of the cost of an asset over its useful life.

- Bad Debts

Amounts owed that are deemed uncollectible.

Reference links

Supplementary resources to enhance your learning experience.