Structure of Final Accounts

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Overview of Final Accounts

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we'll discuss the structure of final accounts. Could anyone tell me what final accounts are?

Are they the financial statements at the end of an accounting period?

Exactly! Final accounts summarize a business's financial performance. They include the Trading Account, Profit and Loss Account, and Balance Sheet.

Why are these accounts important?

Great question! They help stakeholders like investors, creditors, and management assess the company's profitability and financial health.

Is the structure the same for all types of businesses?

Not quite. Sole proprietorships and partnerships have simpler accounts, while companies need additional statements. Remember the acronym 'TPB' for Trading, Profit & Loss, and Balance Sheet!

Got it! TPB stands for Trading, Profit & Loss, Balance.

Exactly! Let's summarize: Final accounts are important for assessing business performance and include Trading Accounts, Profit and Loss Accounts, and Balance Sheets.

Understanding the Trading Account

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let's begin with the Trading Account. Who can tell me its purpose?

Is it to find out the gross profit or loss?

Yes! It shows the gross profit from sales after deducting costs. Can anyone recall what goes into this account?

I remember it includes opening stock, purchases, sales, and direct expenses.

Well done! Always include direct expenses in the Trading Account. Here's a mnemonic: 'SPOPD' - Sales, Purchases, Opening stock, Direct expenses, with Closing stock deducted!

What about gross profit? How do we calculate it?

Gross Profit equals Net Sales minus total costs, which include opening stock, purchases, and direct expenses, adjusted by closing stock. Remember that well!

So gross profit shows how well we manage our production costs?

Exactly! A quick recap before we move on: The Trading Account reveals gross profit or loss using Sales, Purchases, and Direct Expenses.

Exploring the Profit and Loss Account

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now, let's discuss the Profit and Loss Account. Who wants to share its purpose?

It calculates net profit after considering indirect expenses and incomes.

Exactly! Remember, unlike the Trading Account, this account deals with indirect expenses. What expenses might we include?

Salaries, rent, depreciation…

Perfect! Do you notice any pattern in calculating Net Profit?

Net Profit equals Gross Profit plus other incomes minus indirect expenses.

Right again! A helpful mnemonic for this will be 'GIO' — Gross Income Output — showing how Gross Profit funnels into your net income after expenses!

So, stronger sales lead to higher net profits?

Exactly! Your net profit showcases overall business performance. Let's summarize: The P&L Account calculates net profit after accounting for indirect expenses.

Balance Sheet Overview

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

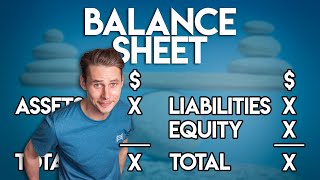

Finally, we will cover the Balance Sheet. What is its purpose?

It shows the financial position of a business at a specific date!

Yes! The Balance Sheet presents assets, liabilities, and owner’s equity. Can someone list the main components?

Assets include what the business owns, liabilities are what it owes, and equity shows the owner's claim on the assets.

Excellent! To remember this, think 'ALE' - Assets, Liabilities, Equity. A simple mnemonic!

How does this relate to the equation you mentioned before?

Good observation! The fundamental accounting equation is Assets = Liabilities + Equity. It’s crucial for balancing the Balance Sheet.

What about the importance of this document?

The Balance Sheet gives insights into financial stability and liquidity, making it critical for stakeholders. Recapping: The Balance Sheet summarizes a business's financial position through Assets, Liabilities, and Equity.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

The structure of final accounts includes the Trading Account, Profit and Loss Account, and the Balance Sheet. These statements provide insights into a business's profitability and financial position, with different complexities for sole proprietorships compared to large corporations.

Detailed

In this section, we explore the structure of final accounts, which mainly consist of three key components: the Trading Account, the Profit and Loss Account, and the Balance Sheet. The Trading Account determines the gross profit or loss during an accounting period, while the Profit and Loss Account calculates the net profit or loss after considering indirect expenses. Lastly, the Balance Sheet provides a snapshot of a business’s financial position at a specific date, detailing its assets, liabilities, and owner’s equity. The accounts of partnerships and proprietorships are simpler, whereas corporations may include more complex statements. Understanding these elements is crucial for stakeholders to assess a business's financial stability and operational efficiency.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Components of Final Accounts

Chapter 1 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Final Accounts typically include:

1. Trading Account

2. Profit and Loss Account

3. Balance Sheet

Detailed Explanation

Final Accounts of a business are structured to include three main components. First, the Trading Account determines the gross profit or gross loss during a specific accounting period. Second, the Profit and Loss Account computes the net profit or net loss after considering indirect expenses and incomes. Lastly, the Balance Sheet presents the financial position of the business at a specific date, summarizing what the business owns and owes.

Examples & Analogies

Imagine you run a lemonade stand. At the end of the day, you would first check how much lemonade you sold and deduct the cost of lemons and sugar used to find out how much profit you made (this is like the Trading Account). Then, you would account for other costs like how much you paid for your stand and other expenses (this is like the Profit and Loss Account). Finally, you would take stock of all your supplies and money to see your total investment and earnings at that specific moment (this correlates to the Balance Sheet).

Final Accounts in Different Business Structures

Chapter 2 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Note: In sole proprietorships and partnerships, these accounts are simple. For companies, additional accounts like Cash Flow Statement, Statement of Changes in Equity, etc., are used under corporate accounting.

Detailed Explanation

The structure of Final Accounts varies depending on the type of business entity. For sole proprietorships and partnerships, the Final Accounts consist of straightforward accounts like the Trading Account, Profit and Loss Account, and Balance Sheet, focusing primarily on essential financial results. In contrast, larger corporate entities, such as public companies, require additional financial statements like the Cash Flow Statement, which provides insights into the company's cash inflows and outflows, and the Statement of Changes in Equity, which shows changes in owners' equity over time.

Examples & Analogies

Think of a small lemonade stand run by a teenager versus a large coffee shop chain. The teenager simply tracks her profit from lemonade sales, which is straightforward. However, the coffee shop chain, due to its size and complexity, needs to track cash movements separately and show investors how much profit is retained versus distributed to shareholders. Thus, while the teenager's accounts are simple, the coffee shop chain needs a more complex structure to satisfy various stakeholders.

Key Concepts

-

Trading Account: Determines gross profit or loss.

-

Profit and Loss Account: Calculates net profit/loss after indirect expenses.

-

Balance Sheet: Shows financial position at a specific date.

-

Assets, Liabilities, Owner's Equity: Major components of the Balance Sheet.

Examples & Applications

Example 1: A Trading Account for a retail shop showing sales of ₹100,000, purchases of ₹70,000, and gross profit of ₹30,000.

Example 2: A Profit and Loss Account detailing indirect expenses of ₹10,000 and net profit of ₹20,000.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

Final accounts are three, TPB, for you to see, profits and losses in a spree!

Stories

Imagine a merchant tallying his sales, juggling opening stock and purchases, he counts his profits, unaware his expenses lurk like phantoms, until the Profit & Loss Account reveals their secrets.

Memory Tools

Remember 'GIO' - Gross Income Output to calculate net profit from gross profit plus incomes minus expenses.

Acronyms

ALE - Assets, Liabilities, Equity — the key components of the Balance Sheet.

Flash Cards

Glossary

- Final Accounts

Financial statements prepared at the end of an accounting period to ascertain business results and financial position.

- Trading Account

An account that determines the gross profit or loss during an accounting period.

- Profit and Loss Account

An account that calculates net profit or loss after accounting for indirect expenses and incomes.

- Balance Sheet

A statement that presents the financial position of a business at a specific date.

- Assets

Resources owned by the business.

- Liabilities

Obligations owed to outsiders.

- Owner’s Equity

Owner’s claim on business assets.

Reference links

Supplementary resources to enhance your learning experience.