Final Accounts – Meaning and Objectives

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Definition of Final Accounts

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Final Accounts are the financial statements created at the end of an accounting period. Can someone tell me why these accounts are significant?

To see how much money the business made or lost.

Exactly! They show the results of business activities. Now, do you know what they consist of?

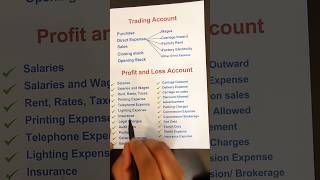

They include the Trading Account, Profit & Loss Account, and Balance Sheet.

Perfect! Those are the key components of final accounts. Remember the acronym T-P-B for Trading, Profit & Loss, and Balance. It can help you remember them.

Objectives of Final Accounts

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now, let’s explore the objectives of final accounts. One goal is to determine gross profit or loss. What does that mean?

It measures how well the company is selling its products after costs.

Correct! Assessing gross profit helps in understanding sales efficiency. Another objective is financial evaluation. Why is this important?

It shows if the business is financially healthy, helping investors and management.

Exactly! These accounts help stakeholders make informed decisions. Let’s summarize: TPG - determining gross profit, P & L evaluation, and ensuring compliance.

Importance of Final Accounts

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Why do you think final accounts are important for a business?

They help in deciding how much tax to pay.

And they help in preparing budgets too!

Absolutely! Final accounts are essential for budgeting, forecasting, tax liability, and they are also used by banks for evaluating creditworthiness. Remember the acronym 'ABCDE' for Auditing, Budgeting, Credits, Decision-making, and Evaluation.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

Final accounts, which are prepared at the end of an accounting period, serve as essential financial statements that help determine gross profit or loss, net profit or loss, and evaluate the financial position of a business to guide stakeholders.

Detailed

In any business, maintaining accurate financial records is crucial for gauging performance and ensuring transparency. Final accounts represent the financial statements prepared at the conclusion of an accounting period. Their purpose is to ascertain the business results and financial standing through a structured summary of financial activities. Key objectives include determining gross profit or loss and net profit or loss, evaluating the financial position through the balance sheet, aiding owners and stakeholders in performance assessment, and ensuring legal and tax compliance. Understanding the structure and components of final accounts is vital for stakeholders like investors, creditors, and regulatory authorities to make informed decisions.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Definition of Final Accounts

Chapter 1 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Final Accounts refer to the financial statements prepared at the end of an accounting period to ascertain the business results and financial position.

Detailed Explanation

Final Accounts are essentially summaries of a company's financial activity over a certain period, usually one year. These accounts help determine how well a business has performed financially—whether it made a profit or a loss—during that period. The phrase 'financial statements' typically refers to structured reports such as the Trading Account, Profit and Loss Account, and Balance Sheet, which are produced at the closing of the accounting period.

Examples & Analogies

Think of Final Accounts as the report card for a student at the end of a school year. Just like a report card shows how well a student did in different subjects, Final Accounts show how well a business did financially over a specific time frame.

Objectives of Final Accounts

Chapter 2 of 2

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

- To determine the gross profit or loss and net profit or loss.

- To evaluate the financial position through the balance sheet.

- To help owners and stakeholders assess the performance.

- To ensure compliance with legal and tax requirements.

Detailed Explanation

The main objectives of preparing Final Accounts are varied and essential for any business. The first objective is to calculate gross profit or loss, which shows how much money the company made from sales after deducting the cost of goods sold. The net profit or loss takes into account both direct and indirect expenses. Secondly, by looking at the balance sheet, stakeholders can assess the financial position of the business at a specific point in time. Additionally, these accounts aid management and owners in evaluating how well the business is performing, allowing for informed decision-making. Finally, adhering to legal and tax requirements is crucial for maintaining the integrity and legitimacy of business operations.

Examples & Analogies

Imagine a coach of a sports team who reviews the season’s performance by looking at scores (gross profit/loss), player statistics (financial position), team training effectiveness (performance assessment), and rules (legal compliance) to plan for the next season. The coach needs all this information to make strategic decisions for future successes, just like how businesses use Final Accounts for their future planning.

Key Concepts

-

Final Accounts: Key financial statements prepared at the end of an accounting period.

-

Gross Profit: Revenue after deducting direct costs.

-

Net Profit: Profit after deducting all expenses.

-

Balance Sheet: Overview of a business's financial standing at a specific point.

Examples & Applications

A retail store prepares final accounts monthly to assess performance and make operational decisions.

A service industry firm uses final accounts annually to evaluate profitability and plan future investments.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

When the business is done, check profits before the fun!

Stories

Imagine a baker checking his ingredients after each day to know how many loaves he can make—this is like final accounts showing a business's financial readiness.

Acronyms

T-P-B helps to remember the Components of Final Accounts.

Flash Cards

Glossary

- Final Accounts

Financial statements prepared at the end of an accounting period to determine business results and financial position.

- Gross Profit

The profit a business makes after deducting the costs associated with making and selling its products.

- Net Profit

The total profit after all expenses, including indirect costs, taxes, and any other costs, have been deducted.

- Balance Sheet

A financial statement showing the company’s assets, liabilities, and capital at a specific date.

Reference links

Supplementary resources to enhance your learning experience.