Balance Sheet

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Purpose of the Balance Sheet

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Welcome everyone! Today we're discussing the Balance Sheet. Can anyone tell me why businesses prepare this document?

Is it to check how much money they have?

That's a good start! The Balance Sheet shows the entire financial position of a business at a specific date. It highlights what the business owns, what it owes, and how much equity the owner holds.

So it’s like a snapshot?

Exactly! Think of it as a snapshot in time. Now, who can tell me what are the three main components of a Balance Sheet?

Assets, liabilities, and owner’s equity!

Correct! Remember the acronym ALOE: Assets, Liabilities, Owner's Equity. Great job!

Components of the Balance Sheet

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now, let’s dig deeper into those components. Who would like to start with assets?

Assets are everything the business owns, right?

That's correct! Can you name some examples of assets?

Land, buildings, and equipment!

Excellent examples! Now, moving on to liabilities. What are they?

Liabilities are what the business owes to others.

Yes! Liabilities can include loans, credit owed to suppliers, and other obligations. And finally, let’s discuss owner's equity. Who can explain that?

It's what the owner claims from the business after paying off liabilities.

Exactly! Owner’s equity represents the owner's claim on assets. Remember, all three components are interconnected as shown in the accounting equation. A good mnemonic to remember is ALOE!

Key Principles of the Balance Sheet

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let’s shift our focus to the fundamental principles of the Balance Sheet. Who can tell me the key equation that governs it?

Assets equal liabilities plus owner's equity, right?

Correct! This is the core of all financial reports. Why do you think this equation is so important?

It helps ensure everything balances out!

Exactly! This dual aspect principle is fundamental. Another important principle is the Going Concern principle, which assumes that a business will continue to operate indefinitely.

What about the Matching principle?

Great question! The Matching principle states that revenues and corresponding expenses must be recorded in the same period. All these principles help create a meaningful financial picture of the business.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

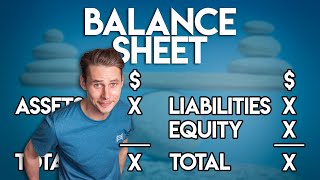

The Balance Sheet is critical for understanding a company's financial position at a specific time. It includes three main components: assets that the business owns, liabilities that represent obligations to outsiders, and owner's equity which denotes the owner's claim on the assets. The fundamental equation governing a Balance Sheet is Assets = Liabilities + Owner's Equity.

Detailed

Balance Sheet

The Balance Sheet is an essential part of the final accounts, illustrating the financial status of a business at a specified date. It encompasses three primary components:

1. Assets: Resources owned by the business that hold economic value.

2. Liabilities: Obligations that the business owes to external parties.

3. Owner’s Equity (Capital): The owner's residual interest in the business after liabilities are deducted from assets.

Key Principles

The Balance Sheet follows the accounting equation:

Assets = Liabilities + Capital

Additionally, it adheres to several accounting principles, such as the Going Concern principle, which assumes that the business will continue to operate indefinitely, the Matching principle, which requires that revenues and their corresponding expenses be recorded in the same period, and the Dual Aspect principle that ensures every transaction affects at least two accounts.

The Balance Sheet is a vital tool for stakeholders (investors, creditors, and management) as it provides insights into the operational health of the business and assists in strategic decision-making.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Purpose of the Balance Sheet

Chapter 1 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

To present the financial position of the business at a specific date.

Detailed Explanation

The Balance Sheet is a financial statement that shows what a business owns and owes at any given point in time. It helps stakeholders, such as investors and creditors, understand the overall financial health of the business. By providing a snapshot of the company's assets, liabilities, and equity, the Balance Sheet allows for better analysis and planning.

Examples & Analogies

Think of the Balance Sheet as a photograph of your financial situation at a specific moment, just like taking a photo of your room to know how it looks before and after cleaning. It helps you see what you have (assets) and what you need to pay (liabilities) to understand your financial status.

Components of the Balance Sheet

Chapter 2 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

- Assets: Resources owned by the business.

- Liabilities: Obligations owed to outsiders.

- Owner’s Equity (Capital): Owner’s claim on business assets.

Detailed Explanation

The Balance Sheet is divided into three main components: Assets, Liabilities, and Owner's Equity. Assets are items of value that the business owns, such as cash, property, and inventory. Liabilities are debts or obligations that the business needs to pay to others, like loans and bills. Owner's Equity represents the owner's investment in the business, essentially what is left after all liabilities are deducted from assets.

Examples & Analogies

Imagine you own a car. The car itself is your asset. If you took out a loan to buy the car, that loan is a liability. The value you have in the car after paying off the loan represents your equity in that car.

Format of the Balance Sheet

Chapter 3 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Liabilities Amount (₹) Assets Amount (₹)

Capital xxxxx Fixed Assets xxxxx

Add: Net Profit xxxxx – Land & xxxxx

Building

Less: Drawings (xxxxx) – Plant & xxxxx

Machinery

Loan (Long- xxxxx – Furniture xxxxx

term)

Creditors xxxxx Current Assets

Outstanding xxxxx – Cash xxxxx

Expenses

Bills Payable xxxxx – Bank Balance xxxxx

– Debtors xxxxx

– Closing Stock xxxxx

Total xxxxx Total xxxxx

Detailed Explanation

The Balance Sheet follows a structured format with Liabilities listed on one side and Assets on the other. This format helps to ensure that the accounting equation (Assets = Liabilities + Equity) holds true. Within each category, there are subcategories. For example, Fixed Assets may include properties like land and buildings, while Current Assets cover cash and inventory. This organized layout allows for quick comparisons and assessments of a company's financial standing.

Examples & Analogies

Consider a balance scale where you place your debts on one side and your assets on the other. Keeping the scale balanced means that for every rupee you owe, you have an equivalent amount in assets. This format helps ensure that your financial 'scale' is even.

Key Principles of the Balance Sheet

Chapter 4 of 4

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Assets = Liabilities + Capital

Must follow the Going Concern, Matching, and Dual Aspect principles.

Detailed Explanation

The Balance Sheet is grounded on essential accounting principles. The fundamental accounting equation states that all assets must equal the sum of liabilities and owner's equity. Furthermore, it adheres to principles like 'Going Concern', which assumes the business will continue operating indefinitely, 'Matching', which aligns expenses with revenues, and 'Dual Aspect', which emphasizes that every transaction affects both sides of the Balance Sheet.

Examples & Analogies

Imagine you own a bakery. The ingredients and equipment represent your assets. The loans you took out to buy that equipment are your liabilities, while the profit you made adds to your owner's equity. Just like in baking, each ingredient must balance with others for the recipe (or financial statements) to come out correctly.

Key Concepts

-

Balance Sheet: A financial statement highlighting a company's financial position at a specific time.

-

Assets: Anything owned by the business that has value.

-

Liabilities: Obligations owed by the business to outside parties.

-

Owner's Equity: The residual interest in assets after deducting liabilities.

-

Going Concern Principle: Assumption that a company will continue to operate indefinitely.

-

Matching Principle: Requires that revenue and expenses be recorded in the same period.

-

Dual Aspect Principle: Every financial transaction affects at least two accounts.

Examples & Applications

A company has assets valued at $500,000, liabilities of $300,000, thus owner’s equity is $200,000.

If a business's total liabilities increase due to a new loan, the owner's equity will decrease unless offset by an increase in assets.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

Assets, Liabilities, and Equity too, Balance Sheet tells what’s owned and due.

Stories

Imagine a store where the owner counts all the things they have, like cash and inventory, but also thinks about what they owe to suppliers. This balance of having and owing is captured in their Balance Sheet, providing clarity on their wealth.

Memory Tools

Use ALOE to remember: Assets = Liabilities + Owner's Equity.

Acronyms

ALO

Assets

Liabilities

Owner’s Equity.

Flash Cards

Glossary

- Assets

Resources owned by the business that provide future economic benefits.

- Liabilities

Obligations of the business that it owes to external parties.

- Owner’s Equity

The owner's claim on the business assets after all liabilities have been deducted.

- Going Concern

An accounting assumption that a business will continue to operate in the foreseeable future.

- Accounting Equation

A formula that represents the relationship among assets, liabilities, and owner's equity: Assets = Liabilities + Owner’s Equity.

Reference links

Supplementary resources to enhance your learning experience.