Types of Financial Ratios

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Liquidity Ratios

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we're diving into liquidity ratios, which are essential for determining a firm's ability to meet short-term obligations. Can anyone tell me the formula for the Current Ratio?

Is it Current Assets divided by Current Liabilities?

Correct! The Current Ratio helps us understand if a company can cover its short-term debts with its current assets. What do we consider an ideal ratio?

It’s 2:1, right?

Exactly! Now, what about the Quick Ratio? Who remembers its formula?

It's Current Assets minus Inventory divided by Current Liabilities!

Perfect! The Quick Ratio is more stringent since it excludes inventory. The ideal here is 1:1. How does this affect our view of liquidity?

It shows a more immediate ability to handle obligations.

Right! Excellent participation. Remember, liquidity ratios help gauge financial health. Let's summarize: Current Ratio is about 2:1, and Quick Ratio is 1:1, excluding inventory.

Solvency Ratios

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Next up, we have solvency ratios. Can anyone tell me what these ratios assess?

They assess a company’s ability to meet long-term obligations.

Exactly! Let’s discuss the Debt-to-Equity Ratio. What’s the formula?

It’s Total Debt divided by Shareholders’ Equity.

Right again! A high ratio here might signal more debt financing. What does that imply?

It could indicate higher financial risk?

Correct! Now for the Interest Coverage Ratio, who can recall the formula?

It's EBIT divided by Interest Expense!

Well done! It measures how easily a company can pay its interest. In summary, solvency ratios project long-term stability, vital for investors.

Profitability Ratios

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let’s look at profitability ratios now. Why are they important?

They show how well a company generates earnings compared to its revenue.

Exactly! Let’s start with the Gross Profit Ratio. Who can share the formula?

It's Gross Profit divided by Net Sales times 100.

Perfect! This shows production efficiency. What about the Net Profit Ratio?

That's Net Profit divided by Net Sales times 100, right?

Absolutely! And it reflects overall profitability. Then we have Return on Capital Employed (ROCE). Who knows that one?

It’s EBIT divided by Capital Employed times 100!

Great! Finally, Return on Equity (ROE) is Net Income divided by Shareholders’ Equity times 100. These ratios give insight into a company's profitability and efficiency in generating returns.

Efficiency Ratios

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Lastly, we have efficiency ratios. Why are they important for a business?

They evaluate how effectively a company uses its assets.

Right! Let's start with the Inventory Turnover Ratio. Can anyone recall its formula?

It's Cost of Goods Sold divided by Average Inventory.

Exactly! This measures how quickly inventory is sold. What does a high turnover indicate?

It implies good inventory management!

Correct! Now the Debtors Turnover Ratio, can someone explain it?

It's Net Credit Sales divided by Average Accounts Receivable, showing how efficiently receivables are collected.

Exactly! Lastly, the Total Asset Turnover Ratio is Net Sales divided by Total Assets. It reflects how effective a firm is at using assets to generate sales.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

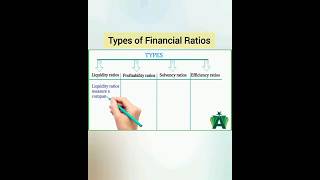

The section categorizes financial ratios into four main types: liquidity ratios, solvency ratios, profitability ratios, and efficiency ratios. Each type serves a unique purpose in analyzing a company's financial statements, helping stakeholders make informed decisions.

Detailed

Types of Financial Ratios

Financial ratios are crucial for interpreting financial statements. They are generally classified into the following categories:

1. Liquidity Ratios

These ratios assess a firm's ability to meet short-term obligations.

- Current Ratio:

- Formula: Current Assets / Current Liabilities

- Ideal Ratio: 2:1

- Interpretation: This ratio indicates whether the company can cover its short-term debts with its current assets.

- Quick Ratio (Acid Test Ratio):

- Formula: (Current Assets - Inventory) / Current Liabilities

- Ideal Ratio: 1:1

- Interpretation: This is a stricter test of liquidity as it excludes inventory, essential for understanding immediate financial health.

2. Solvency Ratios (Leverage Ratios)

These ratios indicate a firm's ability to meet long-term obligations.

- Debt-to-Equity Ratio:

- Formula: Total Debt / Shareholders’ Equity

- Interpretation: A high ratio signals more debt financing, which can indicate higher financial risk.

- Interest Coverage Ratio:

- Formula: EBIT / Interest Expense

- Interpretation: Measures how easily a firm can pay interest on outstanding debt.

3. Profitability Ratios

These ratios assess a firm's ability to generate earnings.

- Gross Profit Ratio:

- Formula: (Gross Profit / Net Sales) × 100

- Interpretation: Reflects efficiency in production or sourcing.

- Net Profit Ratio:

- Formula: (Net Profit / Net Sales) × 100

- Interpretation: Indicates overall profitability after all expenses are factored in.

- Return on Capital Employed (ROCE):

- Formula: (EBIT / Capital Employed) × 100

- Interpretation: Shows efficiency in using capital to generate profits.

- Return on Equity (ROE):

- Formula: (Net Income / Shareholders’ Equity) × 100

- Interpretation: Measures the profit earned on shareholders’ funds.

4. Efficiency or Activity Ratios

These ratios evaluate how efficiently a firm uses its assets.

- Inventory Turnover Ratio:

- Formula: Cost of Goods Sold / Average Inventory

- Interpretation: Measures how quickly inventory is sold.

- Debtors Turnover Ratio:

- Formula: Net Credit Sales / Average Accounts Receivable

- Interpretation: Indicates how efficiently a company collects receivables.

- Total Asset Turnover Ratio:

- Formula: Net Sales / Total Assets

- Interpretation: Shows how effectively a firm utilizes its assets to generate sales.

Understanding these ratios is crucial for evaluating a company’s financial position, particularly for aspiring tech entrepreneurs or managerial roles in tech firms.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Overview of Financial Ratios

Chapter 1 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Financial ratios are generally classified into the following categories:

Detailed Explanation

Financial ratios help assess a company's performance by comparing various aspects of the financial statements. They are grouped into distinct categories based on what they measure, including liquidity, solvency, profitability, and efficiency. Understanding these categories is essential for analyzing a firm’s health and making informed decisions.

Examples & Analogies

Think of financial ratios like different lenses through which an investor can view a company's financial health: liquidity ratios for short-term visibility, solvency ratios for long-term stability, profitability ratios for earning potential, and efficiency ratios for productivity insights. Each lens offers a unique perspective.

Liquidity Ratios

Chapter 2 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

19.2.1 Liquidity Ratios

These ratios measure a firm’s ability to meet short-term obligations.

a) Current Ratio Formula:

Current Assets

Current Ratio=

Current Liabilities

Ideal Ratio: 2:1 Interpretation: Indicates whether the company can cover short-term debts with current assets.

b) Quick Ratio (Acid Test Ratio) Formula:

Current Assets – Inventory

Quick Ratio=

Current Liabilities

Ideal Ratio: 1:1 Interpretation: Stricter test of liquidity, excludes inventory.

Detailed Explanation

Liquidity ratios gauge a company’s ability to pay off its short-term debts using its short-term assets. The current ratio is calculated by dividing current assets by current liabilities, with an ideal ratio of 2:1 indicating that the company has twice as many assets as liabilities. The quick ratio, on the other hand, is a more stringent measure, excluding inventory, and ideally should be at least 1:1.

Examples & Analogies

Imagine you have a monthly budget and expenses. The current ratio is like ensuring that for every dollar you owe this month, you have two dollars ready to spend. The quick ratio is akin to considering only your cash and bank accounts, leaving out any items you might still need to sell to pay your bills.

Solvency Ratios

Chapter 3 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

19.2.2 Solvency Ratios (Leverage Ratios)

These indicate a firm’s ability to meet long-term obligations.

a) Debt-to-Equity Ratio Formula:

Total Debt

Debt-Equity Ratio=

Shareholders’ Equity

Interpretation: High ratio signals more debt financing, possibly more financial risk.

b) Interest Coverage Ratio Formula:

EBIT

Interest Coverage Ratio=

Interest Expense

Interpretation: Measures how easily a firm can pay interest on outstanding debt.

Detailed Explanation

Solvency ratios measure a company's capacity to meet its long-term obligations, primarily evaluating the balance between debt and equity. The debt-to-equity ratio divides total debt by shareholders' equity, indicating the proportion of financing that comes from debts versus shareholder investments. A high ratio suggests increased financial risk. The interest coverage ratio shows how readily a business can pay interest on outstanding debt, calculated by dividing earnings before interest and taxes (EBIT) by interest expenses.

Examples & Analogies

Consider solvency ratios like your long-term financial fitness. The debt-to-equity ratio is akin to how much of your home is mortgaged versus how much you own outright; a high mortgage might mean more risk if your income dips. The interest coverage ratio is like your ability to pay mortgage interest comfortably – if you earn enough to cover the interest payments easily, you’re in a good position.

Profitability Ratios

Chapter 4 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

19.2.3 Profitability Ratios

These assess a firm’s ability to generate earnings relative to revenue, assets, or equity.

a) Gross Profit Ratio Formula:

Gross Profit

Gross Profit Ratio= ×100

Net Sales

Interpretation: Reflects efficiency in production or sourcing.

b) Net Profit Ratio Formula:

Net Profit

Net Profit Ratio= ×100

Net Sales

Interpretation: Indicates overall profitability after all expenses.

c) Return on Capital Employed (ROCE) Formula:

EBIT

ROCE= ×100

Capital Employed

Interpretation: Efficiency in using capital to generate profits.

d) Return on Equity (ROE) Formula:

Net Income

ROE= ×100

Shareholders’ Equity

Interpretation: Profit earned on shareholders’ funds.

Detailed Explanation

Profitability ratios analyze a company's ability to generate earnings in relation to its sales, assets, or equity. The gross profit ratio, which highlights production efficiency, is determined by dividing gross profit by net sales. The net profit ratio shows a firm’s final profitability after all expenses. ROCE gives insights into how well a company uses its capital, while ROE indicates the profit generated per unit of shareholders' equity. These ratios allow investors to gauge how effectively a company is operating.

Examples & Analogies

Think of profitability ratios as indicators of a restaurant's performance. The gross profit ratio can be seen as how efficiently a restaurant turns ingredients into dishes; a high ratio means good kitchen management. The net profit ratio reflects the restaurant's overall health after factoring in all expenses. ROCE is like measuring how effectively the restaurant uses its investment to generate returns, while ROE shows how much profit is generated for each dollar contributed by investors.

Efficiency or Activity Ratios

Chapter 5 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

19.2.4 Efficiency or Activity Ratios

These ratios evaluate how efficiently a firm uses its assets.

a) Inventory Turnover Ratio Formula:

Cost of Goods Sold

Inventory Turnover Ratio=

Average Inventory

Interpretation: Measures how quickly inventory is sold.

b) Debtors Turnover Ratio Formula:

Net Credit Sales

Debtors Turnover Ratio=

Average Accounts Receivable

Interpretation: Indicates how efficiently the company collects receivables.

c) Total Asset Turnover Ratio Formula:

Net Sales

Total Asset Turnover Ratio=

Total Assets

Interpretation: Shows how effectively a firm uses its assets to generate sales.

Detailed Explanation

Efficiency or activity ratios assess how well a company utilizes its assets to generate revenue. The inventory turnover ratio measures how often inventory is sold and replaced over a period, reflecting operational efficiency. The debtors turnover ratio indicates how effectively a company collects money owed by customers. The total asset turnover ratio shows how effectively the company uses its total assets to generate sales, allowing assessment of productivity.

Examples & Analogies

Think of efficiency ratios like a retail shop’s performance metrics. The inventory turnover ratio is how quickly your shop sells its stock; a higher ratio suggests you're quick to bring in sales. The debtors turnover ratio is like keeping track of how fast you collect payments from customers – quick collectors are healthier businesses. The total asset turnover ratio measures how well the shop’s resources, like space and staff, are turned into cash through sales.

Key Concepts

-

Liquidity Ratios: Measure a firm's short-term financial health.

-

Solvency Ratios: Assess a company's ability to meet long-term debts.

-

Profitability Ratios: Determine how well a company generates income.

-

Efficiency Ratios: Evaluate asset utilization in generating sales.

Examples & Applications

A company with $200,000 in current assets and $100,000 in current liabilities has a current ratio of 2:1.

A firm with total debt of $500,000 and shareholder equity of $250,000 has a debt-to-equity ratio of 2:1.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

For liquidity keep your current assets near, a quick ratio of one should be very clear.

Stories

Imagine a small bakery with $200 in cash and $100 in unpaid bills. They can quickly pay off their short-term debts, showcasing good liquidity!

Memory Tools

Remember 'LPS' for Liquidity, Profitability, and Solvency ratios when assessing financial health.

Acronyms

Use 'LEAP' to remember Liquidity, Efficiency, Activity, and Profitability ratios.

Flash Cards

Glossary

- Liquidity Ratios

Ratios that measure a firm's ability to meet short-term obligations.

- Solvency Ratios

Ratios indicating a firm's ability to meet long-term obligations.

- Profitability Ratios

Ratios that assess a firm's ability to generate earnings relative to its revenue.

- Efficiency Ratios

Ratios that evaluate how effectively a firm uses its assets.

- Current Ratio

A liquidity ratio that measures a company's ability to cover its short-term debts with current assets.

- Quick Ratio

A stricter liquidity ratio that excludes inventory.

- DebttoEquity Ratio

A solvency ratio that indicates the proportion of debt and equity in a company.

- Interest Coverage Ratio

A solvency ratio that measures how easily a firm can pay interest on outstanding debt.

- Gross Profit Ratio

A profitability ratio that reflects efficiency in production relative to sales.

- Return on Equity (ROE)

A profitability ratio that measures profit earned on shareholders' funds.

Reference links

Supplementary resources to enhance your learning experience.