Demand

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Understanding Demand

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we will discuss the concept of demand. Demand is essentially how much of a good a consumer is willing and able to buy. Can anyone explain what they think influences demand?

I think it's about the price of the good.

Great point! The price of the good is certainly a crucial factor. We can remember it with the acronym P.I.T. which stands for Price, Income, and Tastes. What are some other factors?

Maybe the income of the consumer?

Exactly! Income directly affects the purchasing power of consumers. When income changes, demand can change too. Any other thoughts?

What about the prices of other goods?

Yes! The prices of other goods, especially substitutes or complements, can have a significant impact. For instance, if the price of butter goes up, some people might buy more margarine instead. That's a shift in demand.

To summarize, demand is influenced by the price of the good itself, other goods' prices, consumers' income, and individual tastes.

Impact of Price on Demand

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Let’s dive deeper into the first variable: the price of the good. How does a change in price affect something like demand?

If the price goes up, then I think people will buy less of it.

Exactly right! This is known as the law of demand: when prices rise, demand usually falls, and vice versa. Can anyone think of an example of this?

Like when the price of avocados went up, I bought fewer!

Perfect example! So, if we keep the acronym P.I.T. in mind, we can better understand how the price of goods interacts with demand.

In summary, as prices increase, demand typically decreases and vice versa.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

In this section, we explore the concept of demand which is the quantity of a good a consumer wants to buy. It highlights that demand is influenced by the good's price, other commodities' prices, the consumer's income, and individual preferences. The section sets the stage for analyzing how changes in these variables impact consumer choices.

Detailed

Overview of Demand

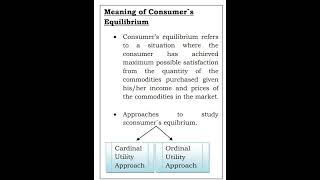

Demand refers to the quantity of a commodity that a consumer is willing to buy at a given price while considering their income and preferences. It is essential to understand that demand is not static; it fluctuates with changes in important variables such as the price of the good itself, the prices of other goods, the consumer’s income, and the consumer's tastes and preferences.

Key Points:

- Optimal Bundle: The optimum bundle for a consumer is determined by their choices in relation to prices and income.

- Variables Affecting Demand:

- Price of the Good: Directly impacts how much of the good is demanded.

- Prices of Other Goods: Can influence demand for a particular good when consumer preferences shift.

- Consumer's Income: Changes in income can make certain goods affordable or unaffordable.

- Tastes and Preferences: Individual consumer preferences can change the demand for various goods.

When any of these variables change, the quantity of goods chosen by consumers typically changes as well. The section aims to study each variable's impact on the consumer's demand.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Understanding Demand

Chapter 1 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

In the previous section, we studied the choice problem of the consumer and derived the consumer’s optimum bundle given the prices of the goods, the consumer’s income and her preferences. It was observed that the amount of a good that the consumer chooses optimally, depends on the price of the good itself, the prices of other goods, the consumer’s income and her tastes and preferences. The quantity of a commodity that a consumer is willing to buy and is able to afford, given prices of goods and consumer’s tastes and preferences is called demand for the commodity.

Detailed Explanation

The section introduces the concept of demand, explaining that it arises from a consumer's choice problem. It clarifies that the quantity a consumer chooses depends not only on the price of that good but also on the prices of other goods, income, and personal preferences. Essentially, demand refers to how much of a product consumers want to buy at a given price, considering their financial ability and desires.

Examples & Analogies

Imagine visiting an ice cream shop where each flavor has a different price. If prices rise, you might choose to buy less ice cream or select a flavor that's cheaper. Your decision reflects demand: how much ice cream you want based on its price, your budget, and your craving for it.

Demand Curve and the Law of Demand

Chapter 2 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

If the prices of other goods, the consumer’s income and her tastes and preferences remain unchanged, the amount of a good that the consumer optimally chooses becomes entirely dependent on its price. The relation between the consumer’s optimal choice of the quantity of a good and its price is very important and this relation is called the demand function.

Detailed Explanation

This chunk defines the demand curve, illustrating that it shows the relationship between the price of a good and the quantity demanded by consumers. The law of demand states that, all else being equal, as the price of a good decreases, the quantity demanded increases, and vice versa. The demand function quantitatively expresses this relationship between price and quantity.

Examples & Analogies

Think of a concert ticket: if the price drops from $100 to $50, many more people might buy tickets. The demand curve illustrates this behavior: the lower the ticket price, the higher the number of attendees.

Deriving a Demand Curve

Chapter 3 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Consider an individual consuming bananas (X1) and mangoes (X2), whose income is M and market prices of X1 and X2 are P1 and P2 respectively. If the price of X drops to P1, the budget set expands and new consumption equilibrium is on a higher indifference curve, demonstrating that demand for bananas increases as its price drops.

Detailed Explanation

This chunk explains how demand curves can be derived from consumer behavior. When the price of a good changes, it affects the consumer's optimal choice, thus demonstrating how demand increases when the price falls. The equilibrium point where the budget constraint intersects with the indifference curve signifies the quantity demanded at a new price level, emphasizing the positive relationship between lower prices and higher demand.

Examples & Analogies

Picture a market sale: if bananas go on sale for $1 each instead of $1.50, more people will buy bananas. The demand curve reflects that as their price decreases, the quantity purchased increases, showing a clear relationship between price changes and quantity demanded.

Law of Demand

Chapter 4 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Law of Demand states that other things being equal, there is a negative relation between demand for a commodity and its price. In other words, when the price of the commodity increases, demand for it falls and when the price of the commodity decreases, demand for it rises, other factors remaining the same.

Detailed Explanation

This section succinctly outlines the law of demand, which asserts that price and demand share an inverse relationship. This principle is foundational to economic theory and highlights how price changes impact consumer behavior, with higher prices typically leading to lower demand and lower prices resulting in higher demand.

Examples & Analogies

Consider gas prices at a fuel station: if the price per gallon rises, you'll likely buy less gas—perhaps only what you need immediately, or consider using public transport. The law of demand explains your behavior in response to changes in price.

Normal and Inferior Goods

Chapter 5 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

For most goods, the quantity that the consumer chooses increases as the consumer’s income increases and decreases as the consumer’s income decreases. Such goods are called normal goods. However, there are some goods the demands for which move in the opposite direction of the income of the consumer. Such goods are called inferior goods.

Detailed Explanation

This chunk introduces two categories of goods: normal and inferior. Normal goods see an increase in demand when consumer income rises, reflecting the consumer's ability to purchase more. In contrast, inferior goods experience a decrease in demand as income rises, as consumers tend to choose better alternatives over these lower-quality goods when they can afford it.

Examples & Analogies

Think of instant noodles as an example of an inferior good. If your income increases, you might stop buying instant noodles and instead choose fresh gourmet meals. In contrast, with an increase in income, you might buy more steak or organic produce, which represents normal goods.

Substitutes and Complements

Chapter 6 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

The quantity of a good that the consumer chooses can increase or decrease with the rise in the price of a related good depending on whether the two goods are substitutes or complementary to each other.

Detailed Explanation

This chunk explains how demand for a product is influenced by the prices of related goods. If two goods are substitutes (like coffee and tea), an increase in the price of one can lead to an increase in demand for the other. Conversely, if goods are complements (like printers and ink), an increase in the price of one can lead to a decrease in demand for the other.

Examples & Analogies

Consider coffee and tea: if the price of coffee goes up, many consumers may switch to tea instead, increasing tea sales. This relationship highlights how the demand for one product can be directly impacted by the price changes of another.

Shifts in the Demand Curve

Chapter 7 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

The demand curve was drawn under the assumption that the consumer’s income, the prices of other goods and the preferences of the consumer are given. What happens to the demand curve when any of these things changes?

Detailed Explanation

This chunk explains that shifts in the demand curve occur due to changes in factors such as consumer income, the price of related goods, or changes in consumer preferences. If income rises, the demand for normal goods shifts rightward, whereas for inferior goods, it may shift leftward. Similarly, changes in the prices of substitutes and complements also affect demand.

Examples & Analogies

Think of fashion trends: if wearing leather jackets becomes popular, the demand curve for jackets shifts rightward as more people want to buy them. Meanwhile, if a harmful study is published regarding the health risks of sugary drinks, the demand for soda may shift leftward as consumers lose interest.

Movements along and Shifts of the Demand Curve

Chapter 8 of 8

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

Movement along the demand curve occurs with changes in the price, while shifts in the demand curve happen due to factors other than price changes, like changes in income or consumer tastes.

Detailed Explanation

This section clarifies the differentiation between movements along the demand curve (caused by price changes) and shifts in the demand curve (caused by other factors). A rise in price leads to a decrease in quantity demanded, represented as movement along the curve, while changes in income or preferences can cause the entire curve to move, showing a new relationship between price and quantity demanded.

Examples & Analogies

Imagine going to buy apples. If the price rises, you'll buy fewer apples—that's a movement along the demand curve. But if you hear positive health news about apples, you may decide to buy more regardless of a price change—resulting in a shift of the demand curve.

Key Concepts

-

Demand: The overall willingness and ability to purchase specific goods.

-

Price: A fundamental factor that shifts consumer demand.

-

Consumer's Income: Directly correlates with the demand for goods, especially luxury items.

-

Tastes and Preferences: Personal consumer choices that affect demand for different products.

Examples & Applications

When the price of a popular video game increases, the demand often decreases as consumers may not be willing to pay more.

If a consumer's income increases, they may purchase more luxury goods like designer clothing.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

When prices rise, demand will fall, what's good for one may not be for all.

Stories

Imagine a shopper at a store with a limited budget. As items get pricier, she must choose less of what she loves, showing how demand depends on price.

Memory Tools

Remember 'P.I.T.' for Price, Income, and Tastes - the keys to demand starts with these.

Acronyms

Demand = W.A.B. (Willingness, Ability, Buy)

Flash Cards

Glossary

- Demand

The quantity of a good that a consumer is willing and able to purchase at given prices.

- Optimal Bundle

The combination of goods a consumer chooses that maximizes their satisfaction within their budget.

- Price

The amount of money required to purchase a good.

- Consumer's Income

The total monetary earnings of a consumer, influencing their purchasing power.

- Tastes and Preferences

The individual likes and dislikes that affect consumer choices.

Reference links

Supplementary resources to enhance your learning experience.