Optimal Choice of the Consumer

Enroll to start learning

You’ve not yet enrolled in this course. Please enroll for free to listen to audio lessons, classroom podcasts and take practice test.

Interactive Audio Lesson

Listen to a student-teacher conversation explaining the topic in a relatable way.

Understanding the Budget Set

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Today, we will explore the concept of the budget set. Can anyone tell me what it means?

Isn't it just what a consumer can afford to buy?

Exactly! The budget set includes all the bundles of goods a consumer can purchase with their income at the given prices. Let’s visualize it. What does the budget line represent?

I think it’s the combinations of goods that use up the entire income?

Yes, that's right! The budget line shows all combinations that cost exactly equal to the consumer's income. Now, remember that it's downward sloping. Why do you think that is?

Because if you buy more of one good, you have to buy less of another?

Good observation! That’s how trade-offs work in economics. Let’s summarize; the budget set allows consumers to understand their choices within financial constraints.

Indifference Curves and Utility

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

Now let’s move on to indifference curves. Who can tell me what they represent?

They show combinations of goods that give the consumer equal satisfaction?

Correct! Each point on the indifference curve indicates a different bundle that provides the same level of utility. What is the slope of these curves called?

Isn’t it called the marginal rate of substitution?

Yes! MRS shows how much of one good you are willing to give up for one more unit of another good. If the budget line intersects an indifference curve, what does that mean?

That means the consumer is at an optimal point of choice?

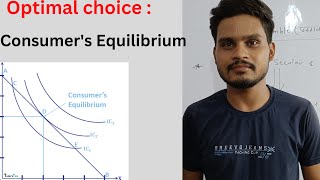

Exactly! It’s where the consumer maximizes their utility given their budget. Remember, the consumer's ideal bundle is at the tangency point between the budget line and the highest indifference curve they can reach.

Market Trade-offs and Rationality

🔒 Unlock Audio Lesson

Sign up and enroll to listen to this audio lesson

So, why do we assume consumers are rational? What does that mean in terms of their choices?

It means they know what gives them the most satisfaction and will choose the best option available.

Precisely! A rational consumer will always select the bundle that grants the highest satisfaction level. How does this relate to our budget set?

They’ll choose the best combination of goods they can afford!

Exactly! Remember, if a consumer is choosing below the budget line, they can find better options on the line itself. Lastly, let’s recap everything we discussed today.

The budget set is defined by what we can afford, the budget line shows the maximum spending, and the consumer aims to maximize utility at the point where the budget line is tangent to the indifference curve.

Well summarized! This understanding is crucial for analyzing demand in the next sections.

Introduction & Overview

Read summaries of the section's main ideas at different levels of detail.

Quick Overview

Standard

Consumers aim to maximize their satisfaction by selecting the optimal combination of goods within their budget. This section details the key concepts of consumer choice, including the marginal rate of substitution, the tangency condition between the budget line and indifference curves, and the implications of these concepts for demand.

Detailed

Detailed Summary

In this section, we explore the pivotal concept of 'optimal choice' that every consumer faces when making purchasing decisions. Key to this discussion is the consumer's budget set, which defines all combinations of goods they can afford based on their income and the prices of those goods. At the crux of their decision-making is the goal to maximize utility, or satisfaction derived from consumption.

The budget line represents the various bundles of goods that exhaust the consumer's income. It is downward sloping due to the trade-off between the two goods; for example, as a consumer buys more of one good, they must forgo some quantity of the other. To identify the optimum consumption bundle, we must consider the marginal rate of substitution (MRS), which indicates how much of one good a consumer is willing to give up for an additional unit of another good, without changing their overall satisfaction level.

The consumer's optimum is found at the point where the budget line is tangent to an indifference curve, reflecting that the rate at which the consumer is willing to exchange goods (the MRS) is equal to the rate at which the market allows them to make that trade (the ratio of the prices). Understanding this equilibrium helps delineate the consumer's demand in response to changes in income and prices for goods, which is further elaborated in subsequent sections.

Youtube Videos

Audio Book

Dive deep into the subject with an immersive audiobook experience.

Choosing the Consumption Bundle

Chapter 1 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

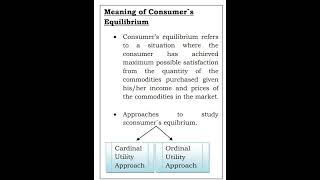

The budget set consists of all bundles that are available to the consumer. The consumer can choose her consumption bundle from the budget set. But on what basis does she choose her consumption bundle from the ones that are available to her? In economics, it is assumed that the consumer chooses her consumption bundle on the basis of her taste and preferences over the bundles in the budget set.

Detailed Explanation

The budget set represents all the possible combinations of goods that a consumer can afford given their income and the prices of the goods. When choosing a consumption bundle, the consumer considers their personal preferences and aims to choose the combination that maximizes their satisfaction within the constraints of their budget. Therefore, the decision is based on their unique tastes, indicating that different consumers may opt for different bundles even with the same budget.

Examples & Analogies

Imagine you're at an ice cream shop with a budget of $10. There are many flavors, but your favorites are chocolate and vanilla. If chocolate is priced at $3 and vanilla at $2, you might choose to buy three scoops of chocolate or five scoops of vanilla, or a mix of both. Your final choice reflects your personal preference for those flavors while staying within your budget.

Marginal Rate of Substitution and Price Ratio

Chapter 2 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

The optimum bundle of the consumer is located at the point where the budget line is tangent to one of the indifference curves. If the budget line is tangent to an indifference curve at a point, the absolute value of the slope of the indifference curve (MRS) and that of the budget line (price ratio) are the same at that point.

Detailed Explanation

The point where the budget line is tangent to an indifference curve is known as the optimum bundle. At this point, the marginal rate of substitution (MRS), which represents the rate at which a consumer is willing to give up one good for another while keeping utility constant, equals the price ratio of the two goods. This equality indicates that the consumer has allocated their budget in the most efficient way possible to maximize satisfaction.

Examples & Analogies

Consider a scenario where you’re deciding between buying apples and oranges. If the price of apples is $2 and oranges $1, and you would be willing to give up 2 oranges for 1 apple, then that’s where your preferences align with the market prices. Finding the balance where your satisfaction (utility) is maximized given your budget is equivalent to reaching the peak of a hill—any point lower means you haven't reached your potential.

Rational Consumer Behavior

Chapter 3 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

In economics, it is generally assumed that the consumer is a rational individual. A rational individual clearly knows what is good or what is bad for her, and in any given situation, she always tries to achieve the best for herself.

Detailed Explanation

The assumption of rationality implies that consumers will consistently make choices that maximize their satisfaction based on their preferences and the constraints they face. They evaluate their options and make informed decisions to choose the bundle that yields the highest utility within their budget, reflecting an understanding of their needs and wants.

Examples & Analogies

Think of a student shopping for textbooks. They will look for books that offer the best value for their education. If one book covers more material and is priced higher, they will weigh whether the additional cost is justified by the increased knowledge they gain. They will rationally choose the option that offers the greatest return on their investment.

Optimum Bundle Location

Chapter 4 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

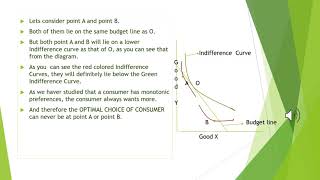

If such a point exists, where would it be located? The optimum point would be located on the budget line. A point below the budget line cannot be the optimum.

Detailed Explanation

The optimum bundle must lie on the budget line because any point below signifies that not all of the consumer's income is utilized, meaning there are options available that provide more satisfaction. On the budget line, every bundle represents combinations of goods that fully utilize the consumer's income, indicating that they are making the best possible purchases with their budget.

Examples & Analogies

Imagine having a $50 budget for groceries. You can choose to only spend $30, but that means you’re leaving some of your budget unspent, potentially missing out on essential items that would improve your meal plan. Therefore, the best outcome maximizes the budget by purchasing a combination of items that fills the entire $50, resulting in a well-rounded grocery list.

Conclusion on Optimal Choice

Chapter 5 of 5

🔒 Unlock Audio Chapter

Sign up and enroll to access the full audio experience

Chapter Content

The optimum bundle is located on the budget line at the point where the budget line is tangent to an indifference curve. All bundles on the budget line are affordable, but only one point provides the maximum satisfaction.

Detailed Explanation

In conclusion, a consumer's optimal choice is the bundle of goods that results in the highest level of satisfaction without exceeding their budget. This is represented by the tangent point on the indifference curve, where the consumer has effectively balanced their preferences with the constraints of their budget, ensuring that they derive the maximum utility from their spending.

Examples & Analogies

Visualize a designer shopping for a dress. They have a budget for $200. While many dresses fall below this price, there’s one dress for $200 that checks all boxes for style, fit, and brand. This point represents their best choice—maximizing their satisfaction within the limits of their budget.

Key Concepts

-

Budget Set: Defines the varying combinations of two goods that a consumer can afford.

-

Budget Line: Graphical representation illustrating the maximum affordable combinations of goods from the budget set.

-

Marginal Rate of Substitution: Indicates the trade-off rate at which the consumer will yield one good for another without loss of utility.

-

Indifference Curve: Represents consumer preferences, showing bundles that offer equal satisfaction.

-

Utility: The satisfaction derived from consuming a product or service.

Examples & Applications

A consumer with a budget of $100 can buy different combinations of goods, such as 10 units of good A and 5 units of good B, provided the prices per unit remain within that budget.

If the price of good A is $5 and good B is $10, a consumer would be able to purchase combinations such as 5 units of good A and 2 units of good B if they wish to balance their consumption optimally.

Memory Aids

Interactive tools to help you remember key concepts

Rhymes

Budget lines are fine, they show what you can buy, trade-offs in mind, always graphing high!

Stories

Imagine a shopper named Sue. She has $100 to spend. She loves bananas and mangoes. As she buys more bananas, fewer mangoes fit her budget, illustrating the trade-offs she faces.

Memory Tools

Remember U.B.L.I. for utility, budget, line, and indifference—key concepts to keep in mind.

Acronyms

B.M.U. - Budget, Marginal, Utility.

Flash Cards

Glossary

- Budget Set

The collection of all bundles of goods that a consumer can buy with their income at the prevailing market prices.

- Budget Line

The line that represents all combinations of goods that cost exactly equal to the consumer's income.

- Marginal Rate of Substitution (MRS)

The rate at which a consumer is willing to substitute one good for another while maintaining the same level of utility.

- Indifference Curve

A curve that represents different combinations of two goods that provide equal satisfaction and utility to the consumer.

- Utility

The satisfaction or pleasure that consumers derive from consuming goods and services.

Reference links

Supplementary resources to enhance your learning experience.